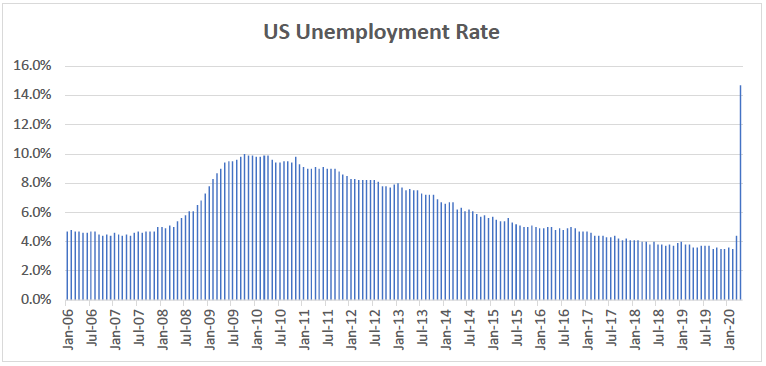

The April employment report was released this morning and the grim tidings it delivered, while anticipated, were still quite startling. The U.S. unemployment rate shot to 14.7%, over 11 percentage points higher than in February, even as the number of payroll jobs in the nation fell by over 20 million. Never has the United States experienced such a dramatic decline in employment in such a short period of time. These numbers would seem to confirm the fears of those who claim that this will end up being not only worse than the Great Recession but perhaps even on par with the Great Depression.

We have cautioned against leaping to such dramatic conclusions. Judging today’s numbers relative to what happened in 2008 and 2009 is an apples-to-oranges comparison. The losses seen then were driven by the permanent collapse of the subprime lending bubble of the previous half decade along with the portions of the economy that had been dangerously overinflated by the massive injection of bad credit. Back then, the most difficult years for U.S. workers occurred after the recession was technically over—unemployment was a lagging indicator.

Today’s numbers are not driven by the permanent collapse of any part of the economy. Rather, they have been driven by the temporary, public health mandated halt in economic activity due to the Covid-19 epidemic. And while a huge part of the U.S. economy has had to close down and furlough workers, there is no reason to assume they cannot or will not reopen once the mandates are lifted. This is why in this particular business cycle, the employment losses not only have happened far more quickly than in past recessions, but they are also a concurrent indicator of economic problems rather that a lagging one.

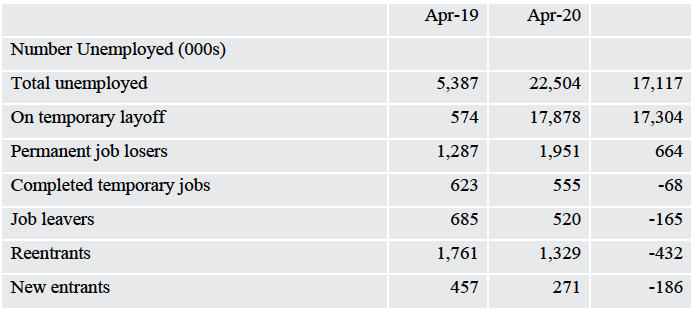

It is easy to call such a view Pollyannaish, but it is largely supported by the data. In April of this year there were 22.5 million unemployed workers in the United States—17.1 million more than in April of 2019. But only 4% of these workers claimed to be unemployed because of a permanent job loss. The large majority claimed they were unemployed because of a temporary layoff. In fact, the increase in the number of people who were temporarily laid off from April 2019 to April 2020 was actually greater (17.3 million) than the overall 17.1 million increase in the number of unemployed.

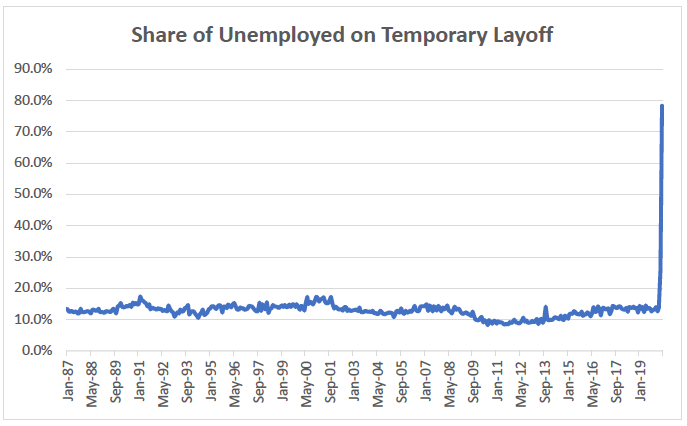

How unusual is this? It is completely unique in U.S. economic history over the last 100 years. Prior to March, the share of the unemployed who claimed to be on temporary layoff was never higher than 20%. In March it was 25%. In April it surged to 75%. In other words—we cannot compare these data to data from 2008 and 2009 and draw any conclusions. This is a different kind of cycle completely.

While many workers hold the view that their job loss is temporary, it’s important to acknowledge that some almost certainly will not find their former job available to them as the economy reopens. This could be due to the business simply not returning to pre-virus staffing levels, or to businesses that fail to reopen at all. The share of jobs that won’t come back is not yet known as the economic damage that would prevent them from returning is only happening right now during the mandated closures. The shape of the recession, “V”, “U”, etc., will depend critically on this.

How many jobs will not return will depend on the five questions we posed in our recent forecast… how long the closures last, how deep they run, how healthy the economy was before the pandemic arrived on our shores, what the government is doing to support the economy, and will there be changes in consumer behavior that will last beyond the public health mandates. As noted in that report, after assessing these questions logically, we believe the majority of jobs will come back, leading to a massive surge in economic activity in the third quarter of this year. This is a “V” shaped downturn, not a “U” or “L”.