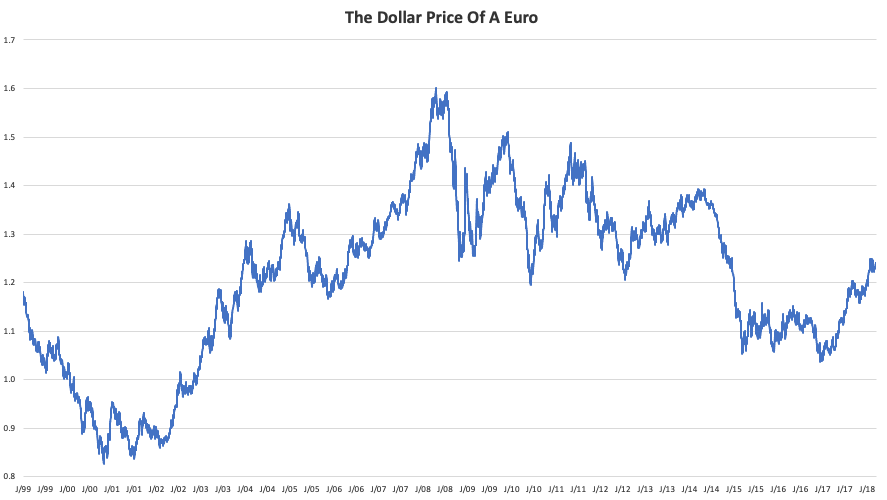

On the 13th of July 2022 the euro broke through parity with the dollar, meaning that one euro traded for less than one dollar. This had not happened in 20 years and is a symbolic testament to the dollar’s strength.

It follows that as the euro currency weakens, exports of goods and services from the Eurozone become more attractive. Indeed, under normal circumstances, a weakening euro would boost European exports and entice foreign investors and tourists. The trouble is that these compensatory market forces are currently unavailable due to heated global economic conditions and the shortages being driven by Russia’s invasion of Ukraine.

The largest Eurozone exporter (Germany) is facing the very real possibility of having to ration energy, including to the industrial sector. European airports are losing half the suitcases checked into airplanes and placing daily capacity limits on the number of flying passengers.[1] Broadly speaking, Europe cannot ramp up its output of goods or domestic services (mainly travel). Europe can export more services, as labor becomes relatively cheaper in the Eurozone. Export services to whom? The United States is the obvious answer. However, “white collar” exportable services have long had a cost advantage in the Eurozone relative to the U.S., and American companies do not appear to be jumping on the opportunity.

Why Should Americans Care About The Euro?

The euro is the second most traded currency in the world, the U.S. dollar (USD) being the first. The Eurozone (the countries using the euro currency) together, represent an economy that is approximately 10% smaller than the United States. Together, the U.S. and European Union (EU)[2] account for 70%+ of global GDP. The euro accounts for approximately 30% of currency trades by volume, USD accounts for roughly 80%, and the Japanese Yen, the next most traded currency, accounts for around 17%. The volume of USD traded is so high precisely because countless financial products and contracts are denominated in USD.

Of course, every dollar traded in the currency market, is traded for another currency. So, in the world of foreign exchange, the dollar or euro themselves are meaningless, what matters is dollars in terms of relative value to the yen, or euro, or renminbi. In other words, a dollar has value in so far as it can trade for something else.

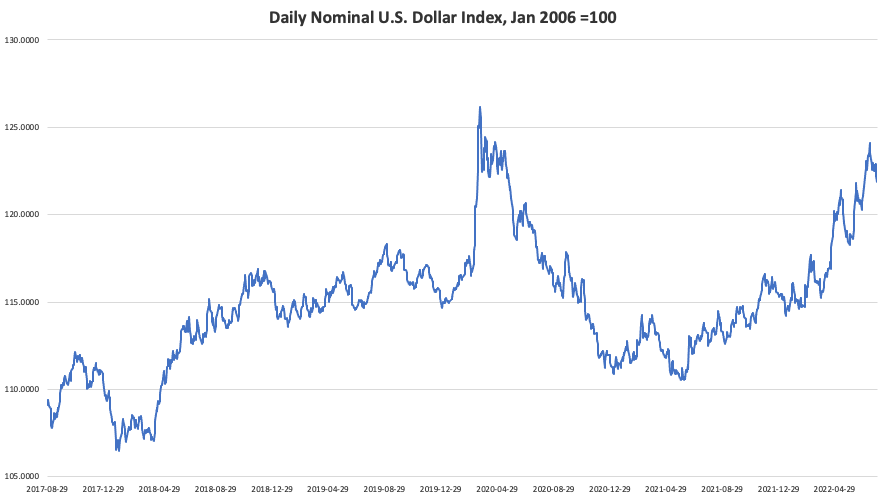

The euro/dollar story is as much about the challenges facing the Eurozone as it is about extraordinary dollar strength. Dollar has always been king. But in these times of volatility and decreased liquidity, it reigns as supreme Emperor. Suppose you run a company with revenues or costs in Korea. The Korean won accounts for only 2% of the foreign exchange market so you may not want to retain this won exposure in times of growing volatility. Hence, you’d convert to a more liquid currency so as to not be ‘stuck’ with a bad position. That liquidity can be found in the dollar.

The dollar’s supremacy is an incredible blessing to the U.S. economy for two primary reasons: its strength is disinflationary, and it keeps government debt yields low.

In terms of slowing inflation, a strong dollar means the United States has a cost advantage in importing goods, particularly commodities which are often priced in USD. For example, the most important crude oil benchmarks are priced in USD, thus any buyer must convert from local currency into USD, creating perennial demand for USD tied to the commodity in question. At times when USD is weaker, foreign countries have an advantage when bidding for oil contracts.[3] A weaker USD will translate to more inflationary pressures arising from the importation of goods – and the United States is a net importer of goods and services.

A strong dollar also maintains the bid on U.S. government debt. A major argument hurled at the size of the U.S. deficit (which is financed through the issuance of sovereign debt) is that servicing the debt (paying interest) will become an undue burden. In fact, many argue that monetary policy cannot get too tight (the Fed cannot raise interest rates too high) as it will unduly aggravate the cost of carrying current U.S. debt. While theoretically it’s true that a higher Fed Funds Rate (what the Fed can actually target) should percolate through all forms of debt, especially sovereign debt, it’s not always the case in practice.

The dissonance between theory and reality lies in the actual plumbing of international trade and capital markets. Economic theories rely on rational agents making rational decisions. We know the first part (rational agents) doesn’t always hold true – but that’s a cheap shot. More importantly, we know the latter part (rational decisions) hinges on market participants’ expectations of the future, and herein lies the beauty (or chaos) of markets: Expectations of the future differ starkly.

Moreover, many participants in capital markets are playing a second or third derivative game. Meaning that they are assuming what the response of the market will be to an event and are willing to take the contrarian position. So, if A -> B -> C, some are willing to go to C, but if enough participants assume others are going to C, they will attempt to bet on the next step D. The over financialization of the economy is evidenced in the wild swings in prices for assets ranging from meme stocks to commodities. Sovereign debt has also experienced above average volatility over the past two years. As the founders of Long-Term Capital Management (LTCM) know, markets can remain irrational much longer than you can remain solvent.

In times of uncertainty, liquid financial instruments win, and of course, as the most liquid asset in the world, U.S. treasury debt is finding lots of bids despite the rising Fed Funds Rate.

We started 2021 with near-zero interest rates extending past the one-year maturity. As the year progressed, the steepening of the yield curve moved to shorter maturity instruments. However, the terminal rate (30 year) barely budged, indicating that there is either (a) a widespread belief long-term yields will be low, or (b) a need by institutional investors to “park” cash somewhere liquid and safe. The former would be the theoretical reason and the latter would be the practical or “plumbing” reason for the low long-term yield. Despite three aggressive rate hikes by the Fed, the 30-year bond only yields 1% more today than it did a year ago.

Bluntly, no one has a good explanation for this. Most individuals would not agree to park money for 30 years to earn a yield of 3%. No less when inflation is running at 9%. Everyone knows this, yet this is the situation we find ourselves in.

We may think the euro does not affect the U.S. economy, but a solution to the Ukraine-Russia-energy crisis situation in Europe will see a sharp rebound in the euro and hence more inflation and higher yields in the U.S. ceteris paribus. In Latin, ceteris paribus means “all else held equal.” Economists love using this qualifier, but of course, when has anything held equal on Earth?

[1] On July 12th, Heathrow Airport asked airlines to stop selling tickets through September 11, 2022; one day later Dublin Airport diverted several flights to nearby Kerry Airport due to staff shortages. Not to be outdone by war and the post-pandemic travel frenzy, climate change is souring the outlook for the Italian Alps with two unusual events: the Po River drying to a trickle, and a July 3rd glacier collapse killed 11 hikers. The Rhine River, an important transcontinental freight route, is experiencing record low water levels such that cargo vessels are unable to sail with full loads. Portugal, sometimes referred to as the “California of Europe” is giving 2022’s Oak Fire a run.

[2] Currently there are 27 European Union (EU) member states (countries), 19 of which use the euro currency.

[3] While the United States has become a net oil exporter since the advent of the shale revolution, the nation still imports a significant amount of oil because most U.S. refineries were made to refine Middle East oils which tend to be significantly sourer and have of lower specific gravity than their American counterparts, namely West Texas Intermediate (WTI) and Louisiana Light Sweet (LLS).