Last year’s COVID-19 stimulus and relief packages enacted by the Federal government played some positive role in helping the U.S. economy weather the pandemic-driven recession that has had such a profound impact on our lives. But it will be counter-productive for the nation to engage in another stimulus package.

Key Points:

- The structure of the stimulus efforts means most of the money will flow into the financial system rather than to current spending, reducing its intended and immediate value of growing the economy and creating new jobs.

- The U.S. economy has already recovered substantially from the pandemic-driven downturn and has plenty of momentum coming into 2021. Moreover, the impact of the first stimulus on savings and bank deposits will provide the necessary fuel to help the nation reach full recovery now that effective vaccines are being distributed and the virus is being brought under control.

- More stimulus will be potentially destabilizing for the U.S. economy. In the short-term. this cash could drive another asset bubble or create inflation. In the longer term, the massive increase in the Federal debt will drive up real interest rates and push the United States significantly closer to a fiscal crisis.

Overall economic activity declined by $1.4 trillion in 2020, and if not for the first stimulus programs, it may have been worse. But these policies also came at an enormous cost, funded by over $3 trillion in new Federal debt. As economists continue to unpack what happened and why, it will become increasingly clear that we earned a very low return on the stimulus funding relative to new debt, something that will cost future generations so much.

The reason for the low returns was driven by any number of factors. Very little of the stimulus was made up of direct spending by the government. Instead, most of the money was transferred directly to households and businesses with the (mostly incorrect) assumption that a majority would be immediately spent on goods and services. But instead of using targeted payments, most of the stimulus was distributed regardless of whether a household or business had suffered any true economic losses from the recession. As such, a very large share of the money ended up filtering through to the financial system in the form of debt reduction, increased savings, or for purchasing stocks, homes, and other assets – all of which are doing little to help those who are truly in need due to the pandemic, or to get an anemic economy back to robust growth.

Thankfully it hasn’t mattered much from a macroeconomic standpoint. The U.S. economy saw a big rebound in production, employment, income, and retail sales after the initial panic, and ultimately performed much better in 2020 than most forecasters first predicted. In real terms, by the 4th quarter the economy was operating at only 2.4% less than it was in the 4th of quarter of 2019 despite the largest surge in COVID cases to date. Earned incomes were up 1.4% from the year before, and combined with the generous increase in government support, overall disposable incomes were up 5% in 2020 over 2019. This recovery makes sense as natural disasters have historically been shown to have limited long-run economic impact despite their tragic short-run consequences. This was never a Great Recession type scenario.

Perhaps even more importantly, the pandemic is in retreat. The number of new cases in the United States has fallen from 230,000 per day to under 100,000 in five short weeks as vaccines are more widely distributed. Beacon Economics anticipates that, short of the emergence of a virus variant that is truly resistant to current vaccines, the U.S. economy will be close to its pre-pandemic trend by the end of the year.

The strength of the rebound itself should be enough to make us question whether we need more stimulus. Of course, this doesn’t align with the steady stream of news stories about labor market blues and struggling households. A recent edition of ‘The Morning’, the New York Times’ daily newsletter, opined that the $1400 cash payments to U.S. households now under debate are justified because “people need the help” – correctly pointing out that there are 10 million Americans currently out of work (David Leonhardt. 2021, January 28. The debate over the checks. The Morning, New York Times).

But without context, that is a misleading metric. There were 5.7 million unemployed in the United States prior to the pandemic when the nation had a 3.5% unemployment rate— a level that is far beyond what economists consider ‘full employment’. So, really, there are 4.3 million excess unemployed, about 2% of the U.S. workforce and less than one-quarter of the 18 million excess unemployed last April. By this metric it is easier to see just how the much the U.S. economy has already rebounded. Moreover, excess unemployment was above 2% for a full five years following the Great Recession, and without stimulus, there was no mass starvation, mass evictions, or major social calamity.

Additionally, over one-quarter of the unemployed today are on temporary layoff—waiting for their job to become available again. If we take these folks out of the mix, the excess unemployment rate has risen to what one might call ‘slightly above normal’ – not quite the existential crisis blaring from headlines on a daily basis. Even if we were to expand our definition to include discouraged workers and the unemployed (the U-6), we still end up with an adjusted excess unemployment rate of 5.6% at the end of 2020. The U.S. unemployment rate was higher than that for 6.5 years in the wake of the Great Recession.

This doesn’t imply that the government shouldn’t help the unemployed and the temporarily laid off, as both are still experiencing a reduction in weekly income. Using the previous metric, the excess number of workers suffering income losses right now totals between 8 and 10 million. But we already have a solution for this—the unemployment insurance system, which, according to unemployment claims data, even with the end of the Federal expansion, is still helping 4.5 million workers in the United States. According to the U.S. Labor Department, when combined with the other expanded programs, there are over 20 million people currently receiving assistance.

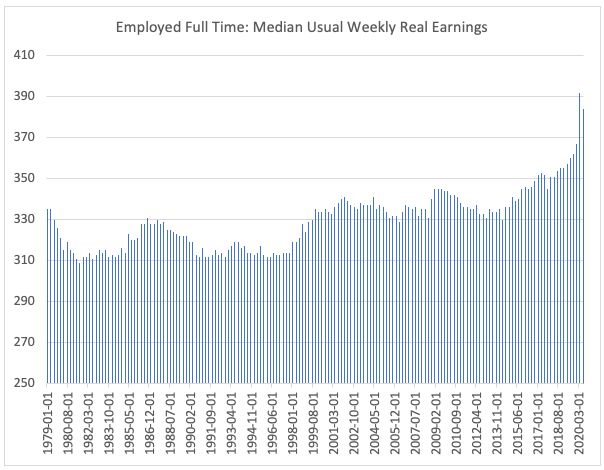

For those who have full time jobs, earnings data suggest that not only have earnings not fallen, but they have grown at a faster pace in 2020 than in the previous year. At the same time, most of the jobs that were lost have been lower paid positions (the hospitality and personal care services industries combined represent over half the pandemic’s job losses). We can see the odd dichotomy: despite an elevated unemployment rate, the job openings rate has barely fallen, and median weekly earnings have shot up dramatically. As such, there was little reason to send checks to 153 million people last year—but we did. To follow this with additional widespread cash disbursements is a complete non-sequitur.

Instead of acknowledging and responding appropriately to the obvious strength of the current recovery, the Federal government is now pushing to spend $2 trillion more on additional stimulus. Worse yet, there doesn’t seem to be any recognition of the specific failings of the earlier policies: They want to distribute the money through the same broad channels that prevented it from being more effective the first time.

It might be easy to shrug and think “better safe than sorry.” But the plan the U.S. government is currently pursuing is not safe. There is the obvious issue of needlessly expanding the Federal debt when really, we should be considering long-run fiscal reforms to deal with expanding entitlement demands. And, of course, the injection of trillions of dollars into the financial system can create instability in inflation, asset prices, and interest rates, dynamics that could end up destabilizing the next expansion and possibly planting the seeds of the next downturn.