Spring 2023

SAN FRANCISCO

Presented by Beacon Economics

Welcome to The Regional Outlook, a forecast for five of the state’s largest metropolitan economies. Each quarter, find updated analysis that goes beyond the state and national level to present a snapshot of employment, home prices, consumer spending, personal income, and other leading economic indicators within key areas of the state. Visit your region of interest and subscribe for email delivery.

Labor Market Growth Slower Than Expected

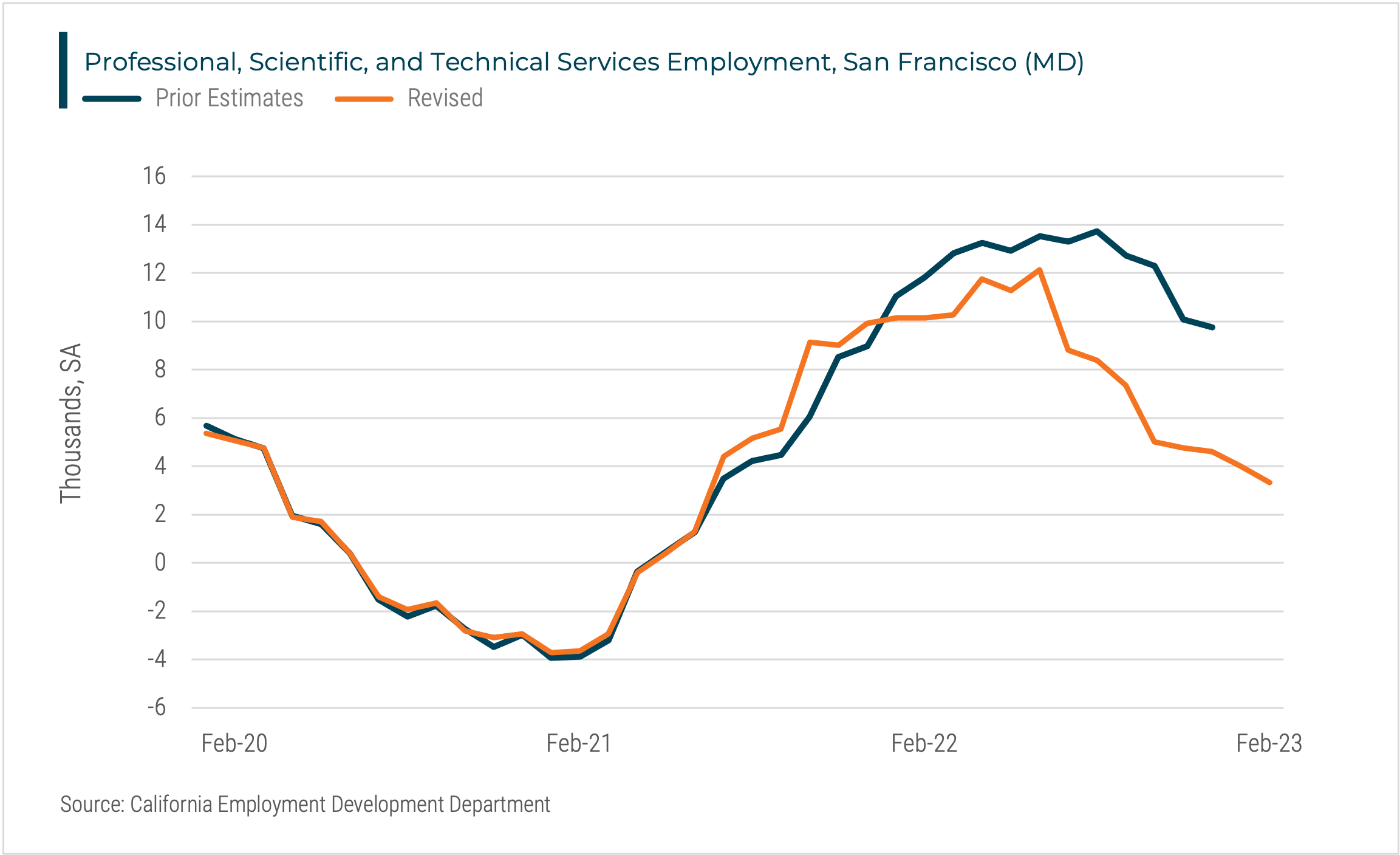

The San Francisco MD (San Francisco and San Mateo Counties) closed out 2022 with noticeably slower job growth than initially estimated. In March, the California Employment Development Department (EDD) released annual benchmark revisions to their monthly employment survey estimates. These revisions indicate that the labor market has been growing slower than originally believed.

Every year, the EDD revises its monthly survey estimates with the Quarterly Census of Employment and Wages (QCEW), which covers roughly 97% of all wage and salary employees in the nation. Prior to the revision, employment in the San Francisco MD increased by 5.3% from December 2021 to December 2022. The revised estimates place employment growth at 3.8%. One industry that saw significant downward revision was the Professional, Scientific, and Technical Services sector, which includes many of the businesses that make up the ‘tech’ sector. Although employment growth came in slower than initially expected, the economy continues to gradually improve, with most major indicators trending in the right direction.

Despite some headwinds, Beacon Economics is maintaining its slow growth/no recession outlook, both nationally and locally. While the labor market provides important insight into the local economy, business and consumer spending is also crucial. When businesses spend money locally, they create jobs, generate income for residents, and contribute to the overall economic growth of a region. This can result in a multiplier effect, as the money spent by businesses circulates throughout the local economy, creating further opportunities for growth. Similarly, when consumers spend money at local businesses, they keep money circulating throughout the community, which can lead to increased employment and business growth.

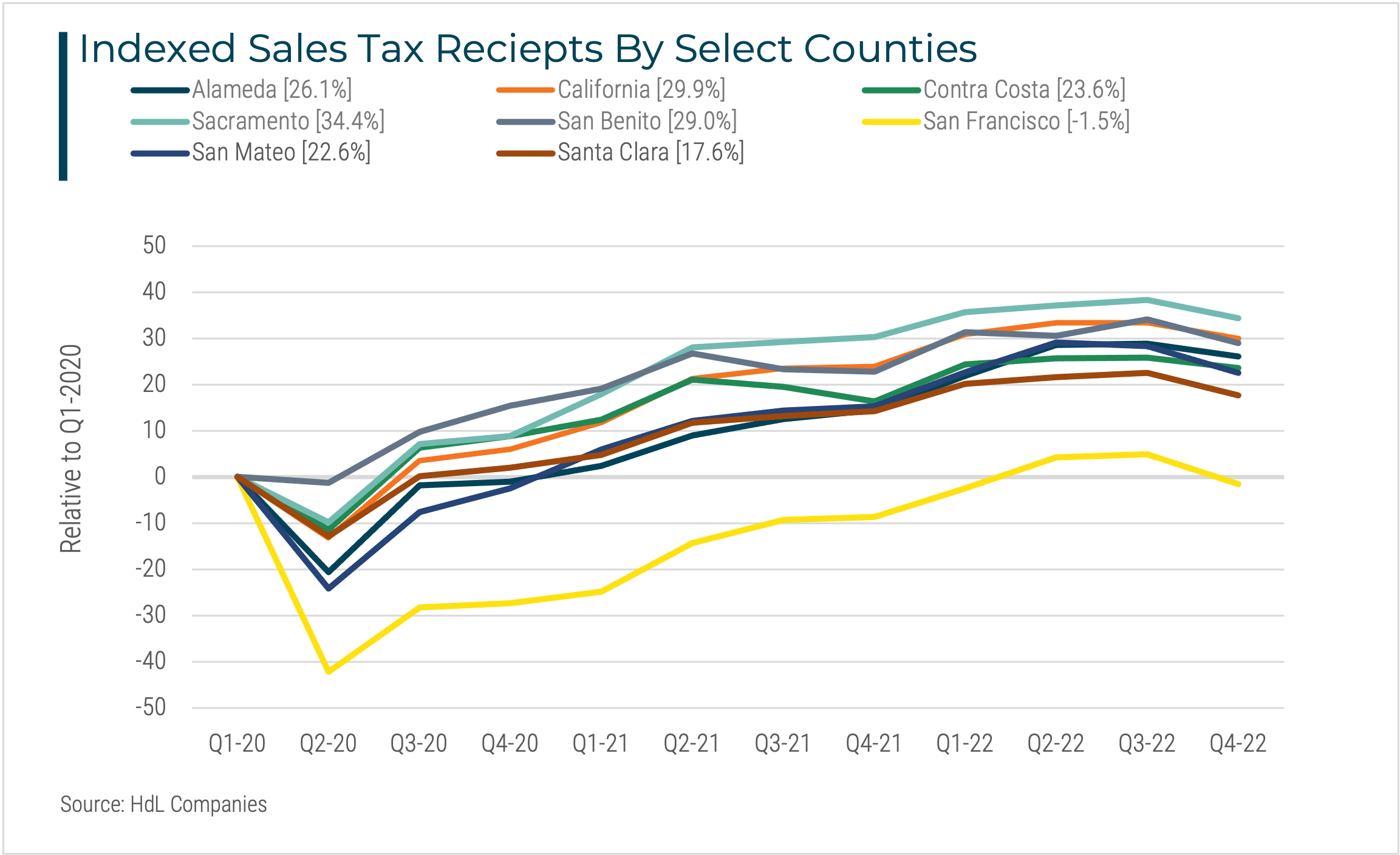

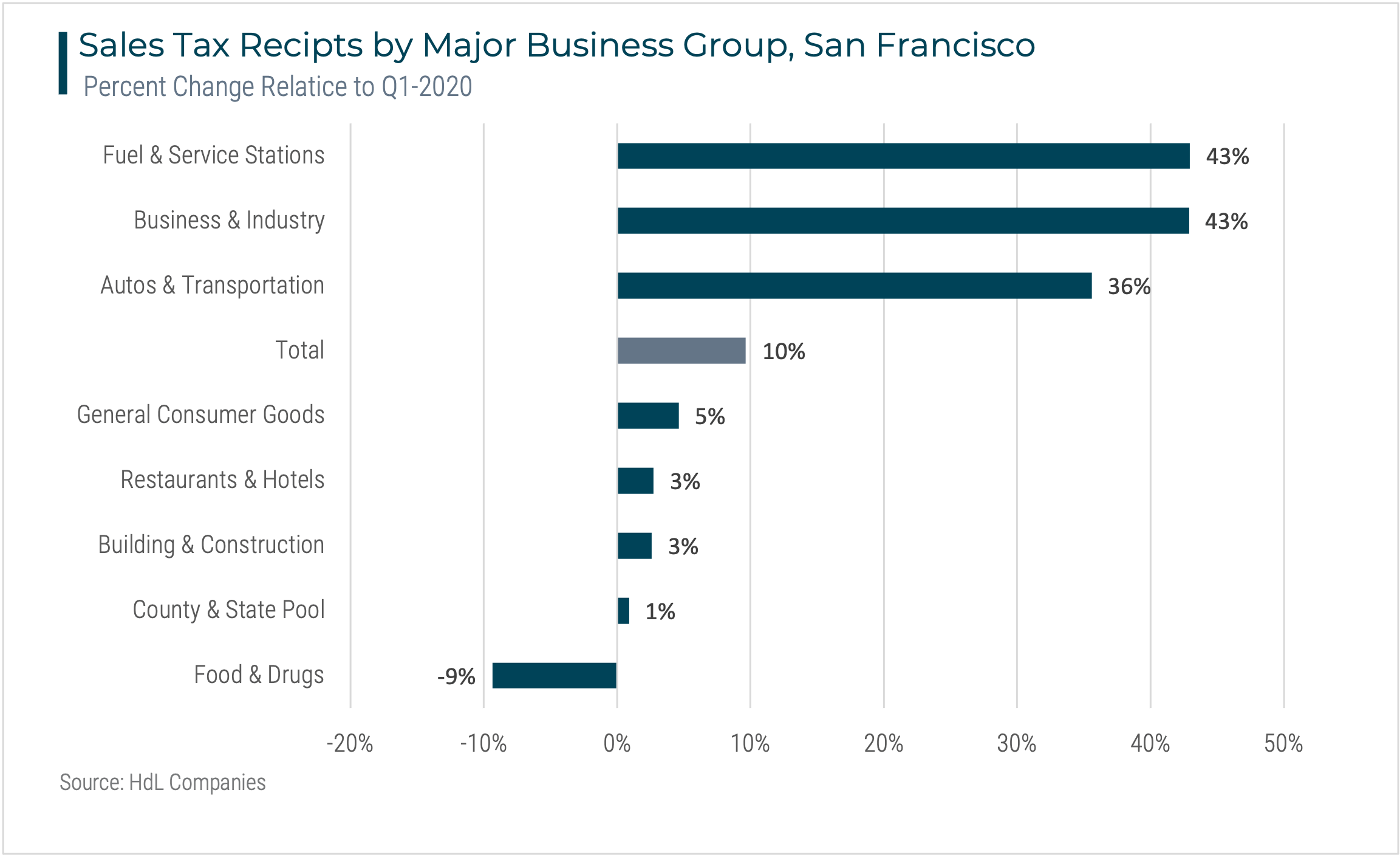

Sales tax receipts data from HdL Companies shows that business and consumer spending has fallen slightly below pre-pandemic levels. Since the first quarter of 2020, sales tax receipts in San Francisco County have declined by 1.5%. This is unique to San Francisco, as nearly all Bay Area counties have experienced a 20%+ increase. A more detailed breakdown of spending in the San Francisco MD shows that nearly every category has increased, especially Fuel and Service Stations, which increased by 53.4%. This jump is unsurprising given the rising cost of oil and the relatively inelastic demand for travel (not as price sensitive).

The weakest category for spending was Food & Drugs, which declined by 9.3%. This category primarily concerns grocery stores, and the decline might not come as a surprise given the decrease in the county’s resident population. Tourism to San Francisco has also been limited, as indicated by the tepid increase in Restaurant and Hotel spending. This weakness also aligns with air travel statistics, which suggest total travel through San Francisco International is still down nearly 30% from pre-pandemic levels. Nonetheless, we still anticipate improvement in the future.

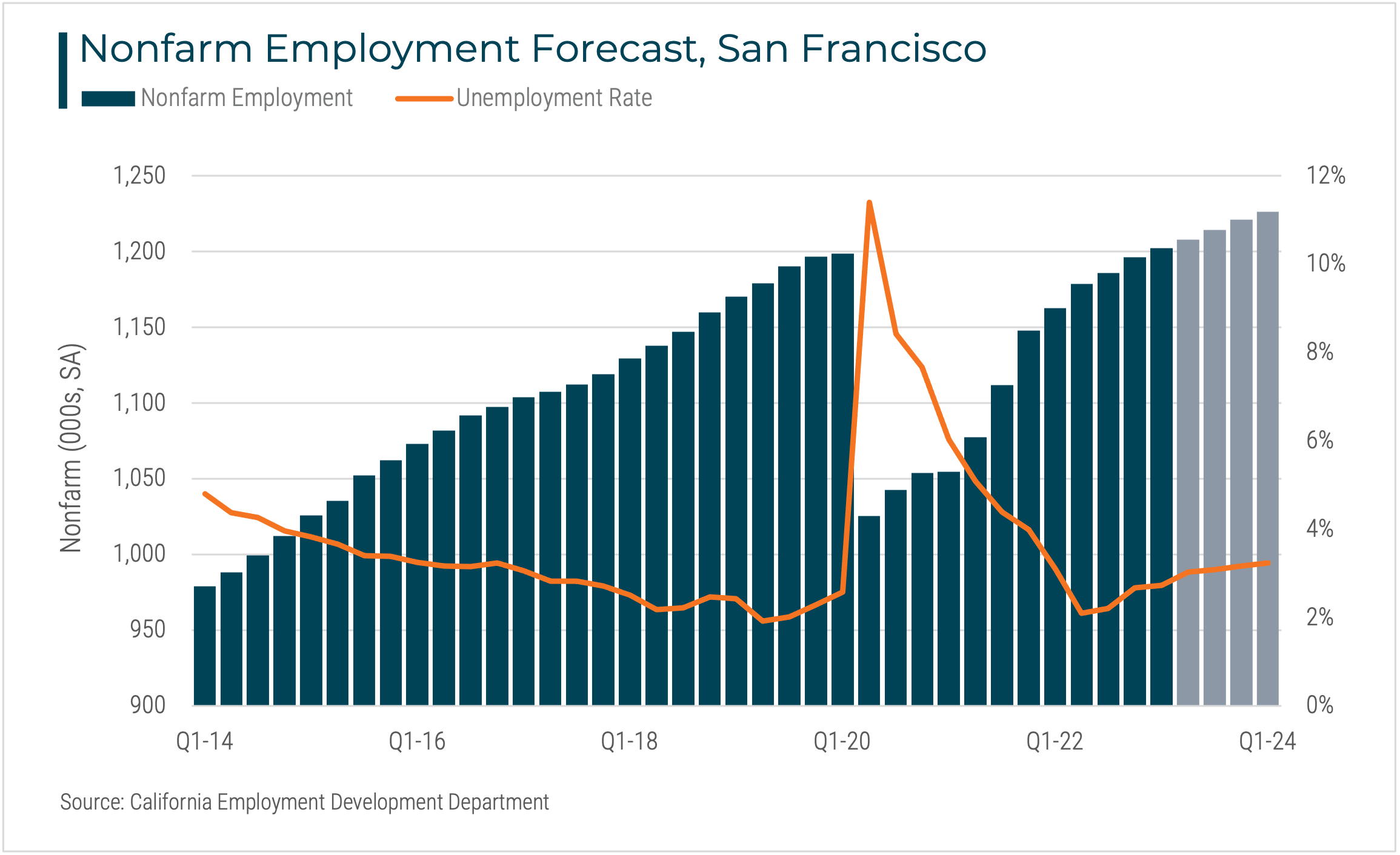

Beacon Economics expects the consumer to keep the economy afloat in the near term, in line with the improvements seen in the labor market. Steady gains in payrolls in the local economy over the last year have driven the unemployment rate down below 3% in the region, a -1.1% decrease from last year. With the unemployment rate back to its pre-pandemic level, and non-farm employment inching toward all-time highs, Beacon Economics is forecasting San Francisco employment levels to continue expanding throughout 2023. Non-farm employment is projected to grow at a steady pace of around 1.5% for the year, while unemployment will likely hover around the 3% mark for the balance of 2023.

Interest Rate Jumps Weaken Housing Outlook

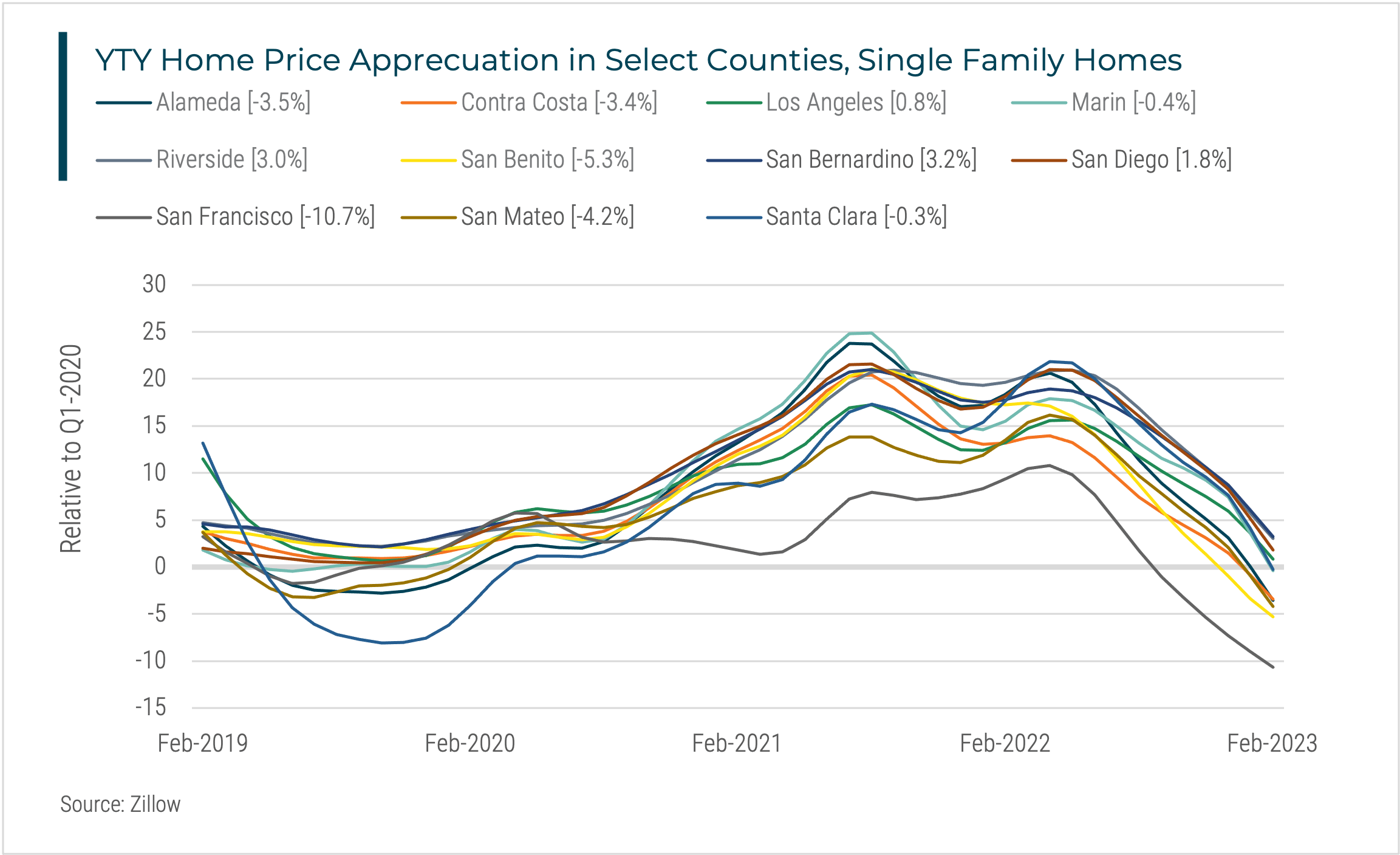

Unlike the labor market, housing continues showing signs of weakness. Rising interest rates have taken a toll on the market, making mortgages more expensive and sidelining would-be homeowners. As a result, home price growth has decelerated, and there has been little relief in terms of new housing production or new inventory of homes on the market. Higher frequency data from Zillow shows a synchronized decline in home price growth, with many markets in California starting to see negative year-over-year growth in home prices.

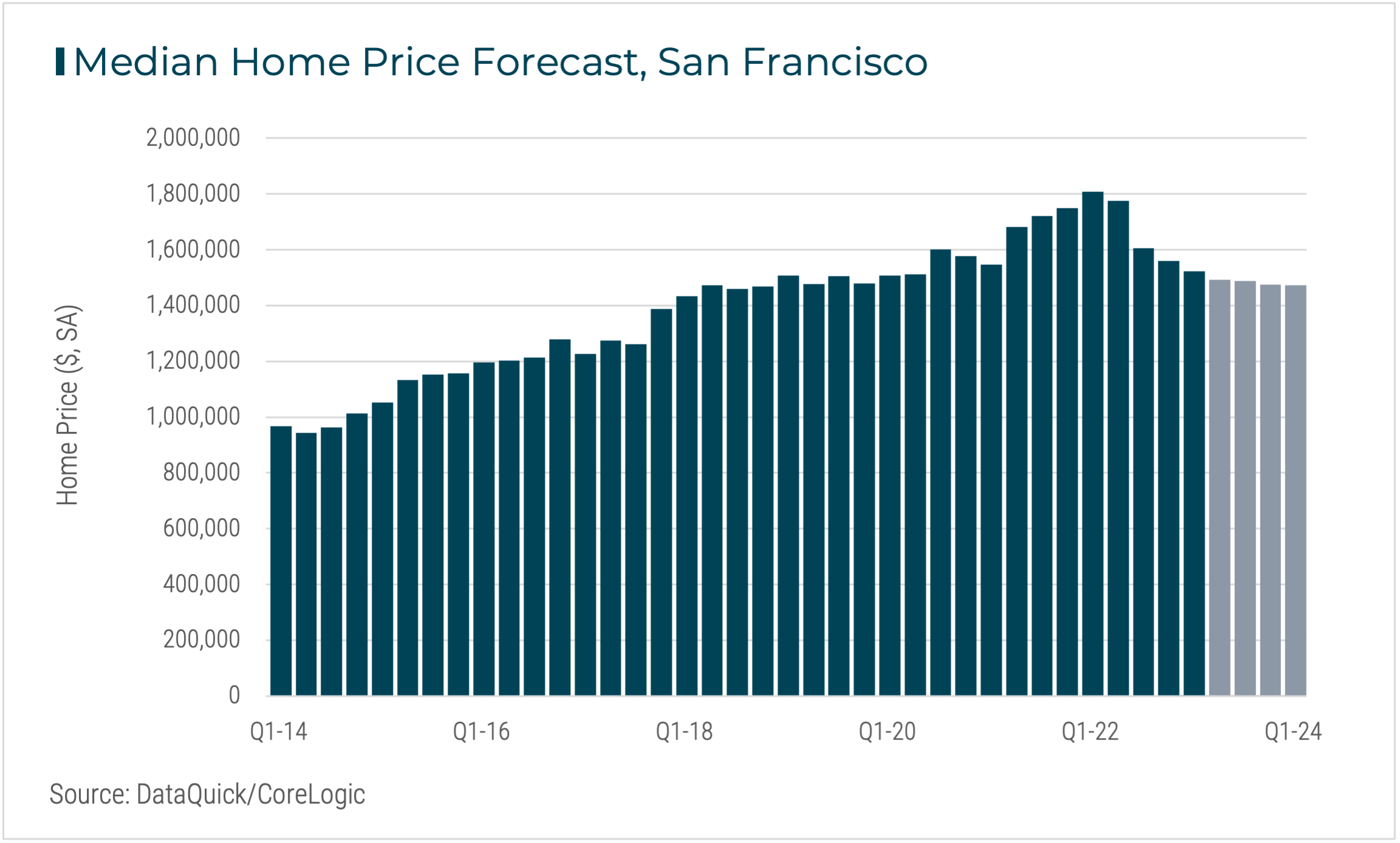

In February 2023, San Francisco home prices had decreased by 10.7% compared to a year ago. At the same time last year, home price appreciation was near double-digit territory. As it stands, there is a very limited supply of homes for purchase on the market. Many homeowners opted to refinance when mortgage rates ticked down to all-time lows during the onset of the pandemic. Since then, the cost of owning a home has risen rapidly, shrinking the number of buyers that can afford to enter the homeownership market and likely keeping many who already own from considering a move – even in high-income San Francisco. As a result, Beacon Economics is forecasting further, although modest, year-over-year price declines in San Francisco’s housing market for the remainder of 2023.

More

Information

For information about any of the Beacon Economics practice areas, please contact:

Business Development Manager Daniel Fowler at 424-666-2165 or [email protected]