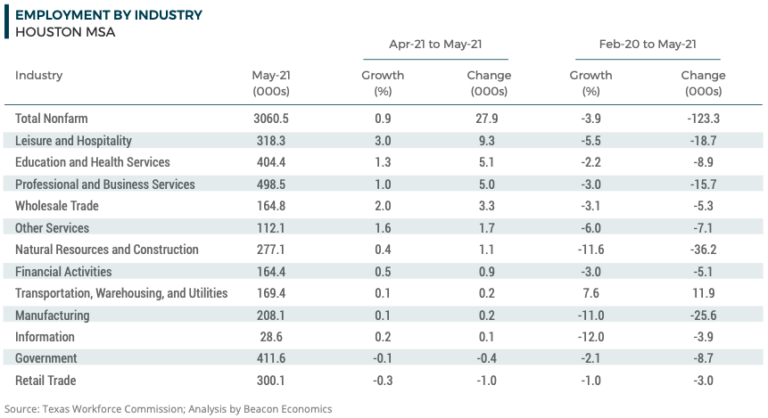

At the industry level, the largest jobs gains continue to occur in sectors hardest hit by the pandemic. The Leisure and Hospitality sector led monthly gains, adding 9,300 jobs from April to May. Next came Education and Health Services (5,100), Professional and Business Services (5,000), Wholesale Trade (3,300), Other Services (1,700), and Natural Resources and Construction (1,100). The few payroll declines in May included Retail Trade (-1,000) and Government (-400).

largest jobs gains continue to occur in sectors hardest hit by the pandemic. The Leisure and Hospitality sector led monthly gains, adding 9,300 jobs from April to May. Next came Education and Health Services (5,100), Professional and Business Services (5,000), Wholesale Trade (3,300), Other Services (1,700), and Natural Resources and Construction (1,100). The few payroll declines in May included Retail Trade (-1,000) and Government (-400).

With Houston continuing to add payrolls in May, the region has now recovered 64% of all the jobs lost in March and April 2020. This trails the 72% job recovery rate in the state overall, and also trails other metros in Texas, including Austin (105%), Dallas-Plano-Irving (MD) (95%), and San Antonio (98%). The trajectory of the recovery among the region’s industries has varied significantly. And although hard- hit industries such as Leisure and Hospitality and Other Services have seen strong growth in recent months, they still have a long way to go to recover all the jobs lost in April 2020’s historic decline.

With the state and region hitting vaccination targets, the restraints on employment growth that were in place at the beginning of 2021 have begun to ease. With more businesses returning to normal operations, Houston will continue to add to its payrolls over the summer.

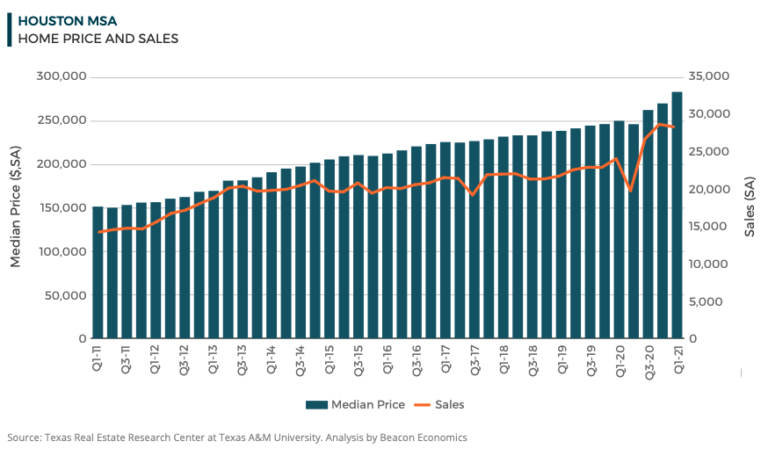

Year-over-year price appreciati on of existing single-family homes in Houston grew 13.3% in the first quarter of 2021. Economic stimulus and low interest rates on mortgages have increased demand for housing throughout Texas. However, supply has not increased to meet these demands. In April 2021, there was only 1.5 months of housing supply in the Houston region.

on of existing single-family homes in Houston grew 13.3% in the first quarter of 2021. Economic stimulus and low interest rates on mortgages have increased demand for housing throughout Texas. However, supply has not increased to meet these demands. In April 2021, there was only 1.5 months of housing supply in the Houston region.

For context, a balanced market typically equates to six to seven months of supply; a buyer’s market equates to seven months of supply and above; and a seller’s market is six months of supply and under (National Association of Realtors). Over the last year, this historically low level of inventory has pushed home prices up considerably, despite a weak labor market and low inflation. That said, the growth in home prices this year will eventually be unsustainable, and an uptick in interest rates should be expected at some point in 2021.

Demand for homes in Houston also remains strong. After the pandemic drove sales down during the second quarter of 2020, they surged in the second half of 2020 and the first quarter of 2021. Existing single-family home sales grew 17.9% in Houston from the first quarter of 2020 to the first quarter of 2021.

Given the underlying strength in the economy, and the increasingly diminished economic effects of the pandemic, a steady increase in the Houston residential real estate market can be anticipated over the next year.