Everything appears to be business as usual when looking at California’s topline jobs number. The state added roughly 32,600 more jobs in 2025 than in 2024, not great, but still an improvement. Today, employment remains at record-high levels, but the source of growth has narrowed considerably, in fact, it’s being driven by a single industry. Removing the Health Care sector from the jobs picture yields an entirely different read on the labor market—without it, California would have fewer jobs today compared to five years ago.

Health Care is playing an increasingly large share in both the state’s and nation’s job numbers. If you exclude Health Care from the mix, the current monthly figures from the U.S. Bureau of Labor Statistics suggest that the United States has nearly 224,000 fewer jobs now compared to February 2025 but because roughly 900,000 Health Care jobs have been added over this period, the nation’s job growth remains positive.

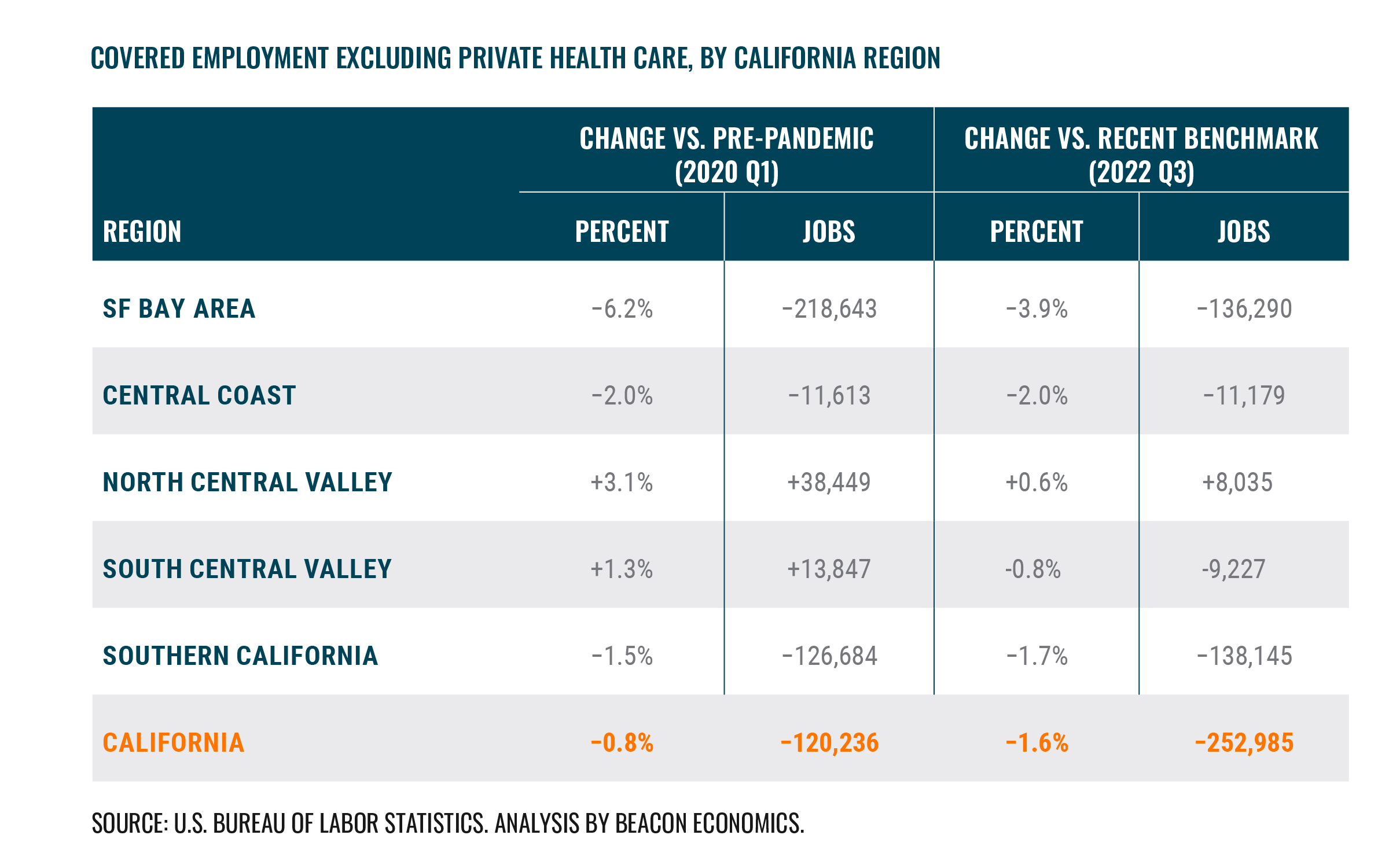

Excluding the Heath Care sector, California’s employment peaked in the third quarter of 2022, the state has lost nearly 253,000 jobs since then, and today still has fewer jobs than prior to the pandemic. This dynamic is occurring across the state’s major regions, and in particular, the large and high-cost metros of Southern California and the San Francisco Bay Area, which collectively shed roughly 275,000 jobs between the third quarter of 2022 and the fourth quarter of 2025. The North Central Valley is the only major region in the state where non-Health Care employment has fully recovered from the pandemic and is above the post-pandemic jobs peak that occurred in the third quarter of 2022.

The growth in Health Care is primarily concentrated at the low end of the wage ladder. In the last two years, one subsector, Individual and Family Services, has accounted for more than half the jobs added in the overall sector. This subsector is the lowest paying in the industry with an average annual wage of $28,370 in 2025. Interestingly, despite claims of a worker shortage, as reflected in California’s weak labor force growth, the subsector doing the bulk of the hiring is the one that pays the least and has a heavy immigrant presence (one-third of workers in Individual and Family Services are foreign born). And this was true throughout 2025, when immigration enforcement sharply intensified.

Aside from the pandemic, Health Care as an industry has largely been recession proof and has rarely experienced declines in aggregate employment. Moreover, demand for health care is largely a function of demographics and policy. California’s population has aged considerably over the course of the last several decades, a trend that will accelerate in the coming years due to falling birth and mobility rates.

On the policy front, California also expanded full-scope Medi-Cal to adults 50+ regardless of immigration status in 2022, and by January 2024, extended coverage to all income-eligible residents between 26 and 49 regardless of immigration status. This is also why Individual and Family Services employment has ballooned recently—the In-Home Supportive Services (IHSS) Program is Medi-Cal funded. In short, the strength in Health Care sector employment is occurring partly because the state is paying more people to care for elderly and disabled relatives. While this still represents positive job growth, it is not the same type of growth that has traditionally supported California’s dynamism. It instead reflects a public reimbursement, not advancement in sectors that are important for broad-based economic growth.

While California’s Health Care sector has been supported structurally by an aging demographic and by public funding, the rest of the state’s economy has seen a sharp reduction in hiring activity. Technology and other Professional Services industries over-hired during the early years of the pandemic, but demand has normalized substantially since then, resulting in both downsizing and a reduction in hiring.

Many sectors are somewhat sensitive to interest rates as well, particularly those that produce goods such as Manufacturing and Construction. Goods producing employment took an initial hit during the pandemic but rebounded shortly thereafter as demand normalized.

Throughout 2021 and into the first half of 2022, goods producing employment in California increased at a solid pace, but the Federal Reserve became more rate restrictive in early 2022. At that time, the effective federal funds rate was 0.08%, but over a span of 18 months the rate increased to 5.33%. Despite the low base, that’s a rapid expansion in borrowing costs and a sharper increase than the rate hikes that occurred in the run up to the Great Recession. Notably, it was during the recent run up that goods producing employment started to turn negative, which is where it stands today even though monetary policy has become more accommodative. Other factors are also at play, especially the Fed’s excessive pandemic-era response which increased the nation’s M2 money supply by roughly 41%, creating the need for rapid monetary tightening.

California’s labor market is also weakening from the supply side. In May 2026, the state’s labor force growth turned negative for the first time since the pandemic. It’s possible these figures will be revised as they are preliminary estimates based on a limited sample of households, but in May, it’s estimated that California’s labor force was down more than 143,000 compared to the prior year.

Despite the decline in the labor force, the labor market is not tight by conventional measures (California’s unemployment rate is among the highest in the nation), and that becomes clear when comparing the number of unemployed persons in the state to the number of active job postings in a given month. Since late 2023, California has had more people looking for work than there are jobs available. The only somewhat positive sign is that the difference between the two measures has not widened. The labor market has not cooled due to lack of workers, but because employer demand has become exceedingly selective and turnover is well below normal rates.

Housing: Frozen At The Top, Thawing Unevenly

The housing market in California has been largely frozen for three years, with minimal movement in sales activity, and that’s not expected to change significantly in the near term. Across all housing types, total sales in California fell by 2.7% in 2025, but with a distinct bifurcation in different segments of the market: resales (existing homes) fell by 0.8% while new home sales declined by 20.5%.

The reason for the softness in the housing market has been a sharp increase in both prices and rates, which have compounded the monthly carrying cost. The monthly mortgage implied by California’s median list price is roughly $4,500 per month, and that also requires a 20% down payment. However, as illustrated in the chart below, conditions have started to improve for buyers, with both median list prices and mortgage rates lower than last year. This should offer some relief as the buying season approaches.

Through the first five months of 2026, housing turnover across California has been limited. Sales activity has stalled out in the more affordable markets, with sales down 6.9% in the lowest quartile. The opposite trend is occurring on the inventory side. Dividing housing markets by price quartile, the most expensive markets are seeing the largest decline in the number of listings. Some sellers have opted to delist their homes, and according to redfin, two of the nation’s top five metros with the largest share of delisted homes were located in California: San Jose and Los Angeles.

Even with a recent softening in prices, homeowners are still sitting on a large amount of equity so many have the ability to walk away from the market if they’re unable to get their asking sales price.

The outlook for California’s housing market is largely unchanged. The market remains frozen but continues to thaw and is not distressed, something that will keep prices from collapsing. A large portion of the ownership market also enjoys low rates, creating little incentive to move. Buyers do have some leverage, but not enough to meaningfully affect prices. While affordability will continue to improve, sales volumes are unlikely to move beyond the levels observed over the last several years.

Commercial Real Estate: A Mixed Bag

Listings for residential might be declining, but the opposite is occurring in California’s commercial real estate market. Across all major commercial property types, vacancy rates are higher today than they were ten years ago. The office market has been exceptionally weak, due to the rise in remote work. As of the second quarter of 2026, the vacancy rate among office properties in the state was 13.8%, higher than the peak office vacancy rate during the Great Recession.

More recently however, over the course of the past year, trends in the office market have improved markedly. In fiscal year 2026, office net absorption, or the change in occupied square feet, moved into positive territory for the first time in years, driven largely by AI-led leasing in the Bay Area. The City of San Francsico, once the poster child for urban decay, saw more than 4 million square feet of new office space leased—and in early June 2026, the city signed its largest office lease since 2018. San Jose and Orange County have also seen significant leasing activity. Overall, the office market appears weak from a vacancy standpoint, but there are signs of improvement in some regions.

A lot has also been made of California’s retail apocalypse, however, retail vacancy rates have only risen by 0.6 percentage points over the past decade. Retail is now the tightest major commercial property type in the state by vacancy rate.

Net absorption for both industrial and flex properties in California was negative for the third year in a row as of fiscal year 2026, and industrial vacancies have continued to climb due to new stock coming online. Indeed, completions for new industrial properties have exceeded 25 million square feet every year for thirteen consecutive years, with current vacancy rates now rivaling Great Recession levels.

Additionally, the trade tariffs imposed by the Trump administration significantly affected China and there has been a sharp decline in that nation’s exports to California. Year-to-date, California imports from China were down 36% compared to the prior year, but overall, the state’s imports are up 5% due to sharp increases from Taiwan, Vietnam, and South Korea. In short, industrial real estate is facing a supply glut, but demand appears to be in relatively good shape.

Conclusion

All these trends suggest that California’s economy is stable but becoming less dynamic in aggregate. The state is still adding jobs, but growth is concentrated in a single low wage Health Care subsector that has been artificially propped up by government policy.

California’s housing market is not collapsing, but there are few signs of improvement in terms of both sales and construction due to the low rates current owners have locked in and the higher rates prospective construction projects face. The total number of building permits issued in 2025 increased compared to 2024 but remained lower than all the years between 2017 and 2023.

The state’s commercial market is bifurcated, with office demand finally ticking up slightly, although that demand has been centered in two Bay Area metros and is not spread across the state. At the same time, an industrial supply glut is working itself off.

California’s economy remains resilient, but its sources of growth have become increasingly narrow. Until hiring broadens beyond Health Care, housing turnover accelerates, and interest-rate-sensitive industries regain momentum, the state is likely to continue expanding—but at a slower and less dynamic pace than has historically defined its economy.