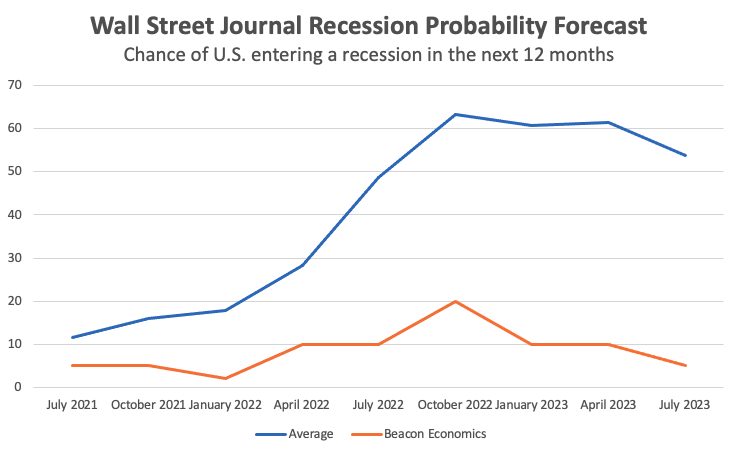

Much to the chagrin of those who have been predicting otherwise, the U.S. economy has stubbornly continued to grow—and 2023 is shaping up to be a better year than 2022. Beacon Economics has argued all along that there is little reason to think we are heading for a near-term recession (outside of our worries about the potential impact of Fed policy). It seems as if our optimism is starting to spread. The Economist recently published an article titled Could America’s Economy Escape Recession?, the latest Wall Street Journal recession probability survey (which we contribute to) shows that economists’ expectations of a recession are starting to fade, and Bank of America became the first major forecast group to retract their recession call.

Beacon Economics recession probability rose only slightly in 2022, and our current estimate of a recession occurring in the next 12 months is at 5%, making us an outlier in the forecast community (take a look at the Journal’s survey and you’ll see what we mean). This isn’t to say that we don’t recognize signs of stress in the economy driven by higher interest rates and the recent bout of inflation. Rather, we’ve never viewed these issues as rising to the level of being systemic given that they were caused by the same thing that has kept consumer spending supercharged—the excessive stimulus thrown at the economy during the pandemic.

The greatest risk, as we have seen it, was always the undue tightening by the Federal Reserve, which was implemented in response to their original sin of excessive loosening. But the nation has fared even better throughout the large interest rate increases than we thought it would. Now, with inflation cooling, the Fed seems likely to slow their credit tightening efforts, so even this concern is fading.

Admittedly, it is affirming to see our optimism playing out in the trends. But what should we make of this big miss by the broader forecasting community? Paul Krugman, in a recent New York Times column, had one answer—forecasters (at least in the aggregate) just aren’t very good at forecasting recessions. He notes that studies of the history of recession predictions show the forecasting community to be remarkably inaccurate—calling for recessions when they don’t occur, and largely failing to predict them when they do. So much for the wisdom of the crowds. But what Krugman never addresses is the ‘why’. Are forecasters just dumb? As John Kenneth Galbraith famously quipped “[t]he only function of economic forecasting is to make astrology look respectable.” Or is there something else going on?

It might seem surprising that forecasters haven’t learned how to predict recessions better, given the technical tools that have been developed over the past 50 years. The first macroeconomic computer model was built by U-Penn’s WEFA group back in the early 1970’s, winning the group’s leader, Lawrence Klein, a Nobel Prize. Today’s economists have far more computing power at their disposal, not to mention a broader set of quality data to play with. Yet, in the aggregate, forecasters still seem unable to see the arrival of the economic tempest until it is already upon us.

The issue with these big macro models is that they are primarily designed to calculate economic trends on the basis of a complex statistical estimate of covariances found within the historical data. Such models rely on each expansion being similar enough to the previous one that these covariances remain relevant. However, recessions are—by definition—a period when the economy deviates substantially from trend. As such, these sorts of forecast models simply don’t have the capacity to predict a recession, unless the forecaster specifically programs it in.

Those seeking to predict oncoming recessions often look for other sets of statistical leading indicators that can foretell when such a break from the trend could occur. In short, they look for historic patterns of data that seem to correlate with oncoming recessions. As it turns out, there are very few of these kinds of guideposts in the data—something that does not surprise us as we’ll explain in a moment. The one data point that does highly correlate with future recessions—and the one that is surely behind the so-far incorrect call of recession by the forecasting community at large—is the inverted yield curve (1). This statistic does indeed have a good track record, with the five recessions prior to the COVID-19 pandemic all preceded by a negative yield curve. Hence, in July 2022 when the yield curve went negative, many forecasters viewed a recession as fait accompli. Yet, as always, conflating correlation with causation is liable to lead to bad calls.

Beacon Economics noted the inverted yield curve last year, but we did not view it as sufficient or even necessary evidence to predict an economic downturn (2). More broadly, we do not believe that there is any recession-predicting “magic bullet” to be found in the data—yield curve or otherwise. To understand our view, start with the recognition that recessions are created by rapid changes in the structure of aggregate demand in an economy. The speed of change is faster than factors of production can be redeployed within that economy. The net result is an overall decline in output and an increase in slack resources—a recession. From this vantage point, predicting a recession means predicting the rapid change in aggregate demand. The key to understanding why there is no clear set of recession leading indicators is recognizing that the sources of recessions are highly varied.

Not unlike Tolstoy’s happy and unhappy families, while every expansion is similar to previous ones (this is the reason VAR models are good at predicting trends), every recession is liable to be significantly different from previous ones. There is a broad range of potential causes behind a rapid change in aggregate demand, from various forms of financial bubbles that will eventually pop, to bad government policy choices, to truly random events like global pandemics. Each type of recession driver has its own specific set of leading indicators compared to others. Add the additional facet that people are unlikely to make the same set of bad decisions that led to some economic calamity in the past, making it even less likely that two recessions will have similar leading statistical patterns (3). Thus, relying on simplistic indicators will inevitably lead forecasters astray.

To appreciate this issue in the extreme, consider a situation where there can be no true leading indicators. In March 2020 when COVID-19 was spreading rapidly through the United States, it became clear that governments would be enacting strict public health measures to control the spread of the malady, and that these efforts were going to close a large portion of the service sector. It was pretty obvious that the U.S. economy was going to experience a recession, since this is exactly the type of rapid change in aggregate demand that drives recessions. But given the sheer randomness of the emergence of viral pandemics, there simply can be no economic leading indicator.

Of course, most recessions don’t begin so arbitrarily. In 2006 Beacon Economics was the first West Coast forecast to predict what eventually became known as the ‘Great Recession’, a destructive downturn that started in the 1st quarter of 2008. The roots of that recession were manmade in the form of a massive subprime consumer lending surge that started in 2003 and vastly overheated both the housing market and consumer spending. By 2006 it was clear that these imbalances had moved way past the point of no return and the economy would necessarily experience a recession—driven by rapid declines in the housing supply and consumer spending—once the sub-prime bubble inevitably collapsed in on itself. The imbalances were the leading indicators. Yet, we know that these imbalances were different than the ones that led to the tech downturn in 2000 (a stock market bubble combined with excessive business investment) or the 1991 downturn, which was driven by excesses in bank lending and commercial investments.

What all three of these recessions did have in common was the inverted yield curve, including in 2006 when Beacon Economics made its early call of the Great Recession. Ironically, at that time forecasters were more skeptical of this statistical bad omen. One article written at the time from U-Penn, home of the legendary WEFA model, stated that the inverted yield curve “… gave shudders to those who see the phenomenon as a harbinger of recession. And yet, the U.S. economy is strong, and surveys show most forecasters think it will stay that way.” In the first half of 2007 the Wall Street Journal recession probability survey was running 25%, as opposed to the 60% level during the first half of 2023.

Perhaps it was their bad call in 2006/7 that made more forecasters believe the yield curve indicator. Why hasn’t it worked for the current recession predictions? Inverted yield curves are primarily generated by the Fed’s choice to push up short-term interest rates. Back in 2006, short-run rates were pushed higher because the Fed was worried about consumer lending and the housing market. In the 2000 downturn, it was because the Fed was worried about the tech stock bubble. In these cases, the inverted yield curve can be thought of as nothing more than skid marks up to the edge of a cliff, created by a driver who realizes, belatedly, of the approaching danger. In contrast, in 2022, short-run rates were raised because the Fed was worried about inflation. But inflation by itself has never caused a recession. And as for the rest of the U.S. economy, there are no major imbalances as there were in 2006 or 2000. The link between the inverted yield curve and a true recession-causing imbalance in the economy wasn’t there this time.

But there is a deeper issue at play. The types of imbalances that ultimately end up collapsing, and cause recessions, are typically driven by narratives that, at least in hindsight, are clearly false. The tech bubble was driven by the “New Economy” narrative, while the Great Recession was driven by Wall Street’s magical alchemy that pretended to convert subprime debt into safe investments. Nobel Prize winning economist Robert Shiller notes in his book Irrational Exuberance “[h]ow errors of human judgment can infect even the smartest people, thanks to overconfidence, lack of attention to details, and excessive trust in the judgments of others, stemming from a failure to understand that others are not making independent judgments but are themselves following still others—the blind leading the blind.”

The fact is forecasters are human and just as likely as anyone to be swept up in a collective madness of broken narratives. William Bernstein, in his recent book The Delusions of Crowds, writes that the author of one of the earliest analyses of recession-causing bubbles, Charles Mackay, largely failed to recognize the bubble he was living in while writing his book. Mackay’s missive, Extraordinary Popular Delusions and The Madness of Crowds, was first issued in 1841 and examined the South Sea and Mississippi bubbles that had rocked the British and French two decades prior. Yet, he failed to see the crazed trading surrounding railroads that ended up causing massive damage to the British economy in the Panic of 1847.

One could suggest that if a narrative can actually cause a recession, it has to have the capacity to sway forecasters. But such a claim may be justifiably called self-aggrandizing, as it relies on forecasters actually having social and political clout. But, given what we have suggested above, this may well be by definition. In such a world, we have to rely on Warren Buffet’s famous line to be “fearful when others are greedy, and greedy when others are fearful.”

Ultimately, recession forecasts can only be created through a complex interaction of theory and data to identify when and where economic trends become so disengaged from normality as to ensure a recession when the process does eventually begin. Of course, such a determination is full of nuance and subtlety. Beacon Economics made the right call in 2006 because the signs of excess were, at least in our estimation, glaring. We made the right call in 2022 because there were few signs of such excess. We haven’t yet been tested by a less obvious situation. As the disclaimer goes, past results are no guarantee of future returns! Forecasting truly is an art. But I still believe we have a leg up by always keeping in mind not just what the data can tell us, but also what it can’t.

(1) The yield curve is the difference between short and long run interest rates. In the past, when short run rates are higher than long run rates, we say the curve is inverted.

(2) We can proudly state that the only two times Beacon Economics has predicted a recession was back in 2006 at the firm’s inception – I left the UCLA Anderson Forecast in 2006 to found Beacon in large part because I thought the real estate bubble would cause a recession upon its collapse, a point of view not welcomed by the UCLA Forecast’s director – and in March 2020 when it became obvious the pandemic had spread globally.

(3) This is a version of the Lucas critique, which says once we make a big mistake we are unlikely to do it again, as we should have learned from our error. This implies that, statistically, the chance of back-to-back recessions looking the same is less than pure probability would suggest.

Beacon Economics specializes in delivering top down outlooks for local economies, government and industry revenues, population dynamics, and other key metrics vital to public and private sector decision making. Our forecasts are used by states, counties, cities, banks, investors, unions, nonprofits, and major industries. Learn more.