As Beacon Economics has written in our published outlooks over the past six weeks, a true understanding of what is currently happening in the economy is limited given the delay in receiving relevant data, as well as the total lack of recent historical examples illustrating how pandemics impact economies. As such, any prediction of how the COVID-19 crisis will affect the economy over the next year should be presented with the utmost humility—advice that the vast majority of forecasters seem to be ignoring in their increasingly hyperbolic predictions of economic collapse.

It simply isn’t that clear. While we appreciate that the numbers on jobs and economic activity are grim, they are not being driven by true, structural economic problems, but rather public health mandates. Once the mandates are lifted, there is no reason to assume that things won’t quickly get back to normal. The depth and degree of the economic damage will be determined by the five questions detailed in our recent outlook. We believe that true, long-term damage will be minimal, and we anticipate a strong rebound in the second half of the year (a “V” type business cycle).

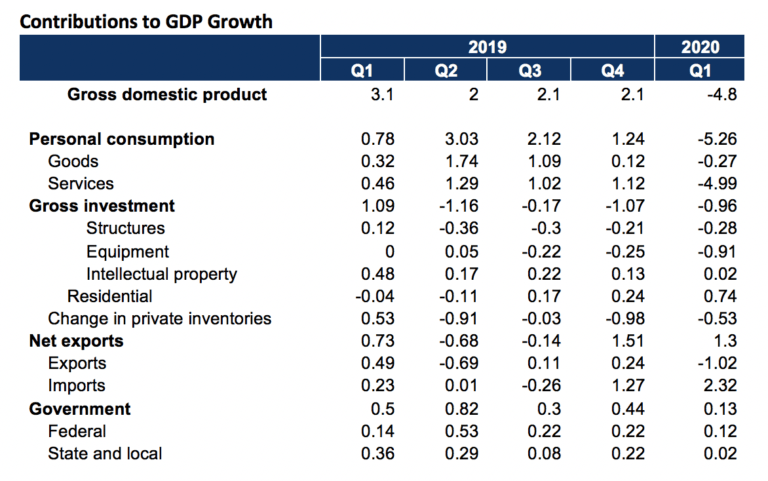

This week, the first estimate for first quarter GDP growth was released—and it isn’t pretty. The economy contracted at a 4.8% pace, driven by a very sharp decline in real consumer spending. This is not as bad as it sounds, since (as always) growth is presented in annualized form. In real terms, it means that economic activity contracted by about 1.2% from the fourth quarter of 2019 to first quarter of 2020, driven by a less than 2% decline in spending. But it still represents the third worst showing for the economy in over three decades and worse than what Beacon Economics anticipated. This means, almost assuredly, that the record long economic expansion that began way back in July of 2009 will be officially declared over as of February of this year—whenever the National Bureau of Economic Research gets around to officially dating the cycle.

It’s easy to look at the first quarter GDP number and assume it confirms much of the negative rhetoric that has been dominating headlines. But digging into the data actually suggests a more positive story. As such, Beacon Economics is sticking with our outlook for the post-virus U.S. economy: a sharp downturn where the record negative number we will surely see in the second quarter (the estimate will be released in late July) is followed by a record positive number in the third quarter as the economy surges towards a more normal level of output.

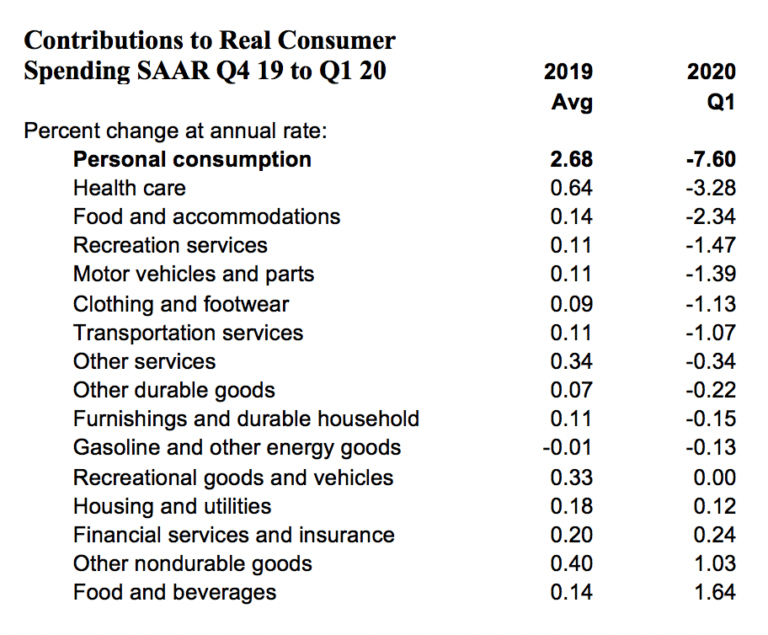

One bit of good news comes from the sources of contraction in the first quarter. We correctly predicted that the decline in spending would negatively impact the travel, food, recreation, and auto industries, but these hits were not large enough to explain the full pullback in consumer spending last quarter. Digging more deeply into the spending data, it’s evident that the largest pullback in the economy—one that explains nearly half the decline in first quarter economic output—is, paradoxically, health care.

The recent decline in spending is being driven largely by the industry’s decision to put all but medically necessary procedures on hold, both to create capacity for the expected surge in virus-related demand as well as to avoid the close mixing of patients with COVID-19 and those seeking other sorts of medical assistance. We had anticipated that accelerated health care spending driven by the need to care for those who contracted and became ill from COVID-19 would offset this decline. It clearly didn’t.

The decline in health care spending, however, is actually good news for two reasons. First, it presents clear evidence that the health mandates are working. Outside of New York and Seattle, there have been almost no hospitals that have struggled with excessive demand from those needing medical care due to complications from COVID-19. And with the number of new cases declining, for now it appears that the industry will not have to worry about the ability to manage demand.

The second reason the decline in spending is positive news is related to the intentional decision to defer non-emergency care. The sharp pullback in health care spending is truly unique. This sector has been growing consistently for decades and has largely been immune to the business cycle; there were no declines in health care spending throughout the Great Recession. Much of the industry is funded only indirectly through consumers with other payments and funding coming through insurance or the government. Medical procedures are not something most people skip altogether or permanently. All those delayed teeth cleanings, eye appointments, and other health procedures will happen, just later in the year. This supports the “V” outlook, with a surge in health spending as people catch up on basic needs. It is also worth noting that the easing of restrictions in California is beginning with health services, which will help second quarter numbers.

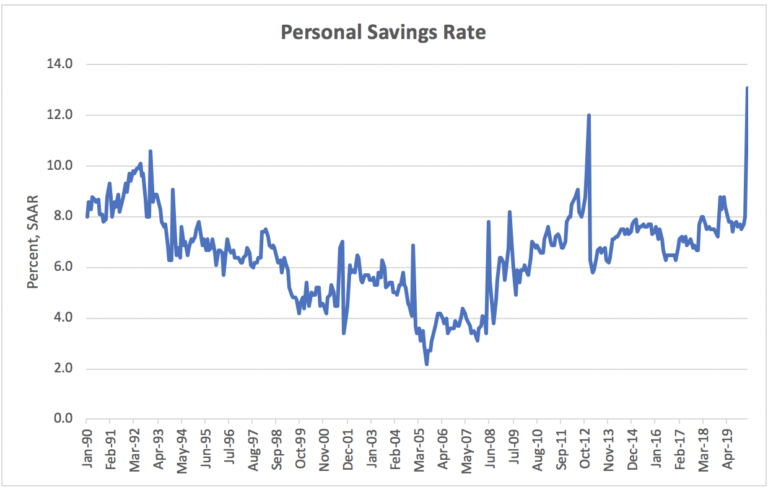

Another bit of good news comes from the income numbers. Many workers and business owners are suffering from lost income—losses that will constrain their ability to spend after the health mandates are lifted (one reason those predicting a “U” are calling for a slow, delayed recovery). But many other workers are not experiencing the same degree of income impairment and are instead being denied the ability to spend their income due to the shutdowns. This will lead to increased savings among these households and pent up demand. If the second effect is greater than the first, on net, it will generate excess spending in the second half of the year.

The March savings rate—when the restrictions went into place—leaped to 13.1%, the highest in decades. At least for now, pent up demand in the form of unspent income is clearly greater than lost income among those who have been economically affected, again supporting the “V” recovery theory. April numbers, however, may be more telling because the income hit may be lagging. Clearly, there is still a long way to go and a lot of uncertainty related to the overall path of the virus and the mandates that are causing harm to the economy, but Beacon Economics continues to believe that as far as recessions go, this will be a dramatic but short lived one.