Author

The recent downward revision of U.S. job numbers is very likely the real deal and reflects an intensifying labor shortage. The U.S. economy needs workers and will only attract them through healthy immigration. That doesn’t bode well for at least the next three years.

The recent revision was also not a politically motivated conspiracy, and that can be seen in the history of the numbers. But the unusually large drop does reflect long standing technical issues with the way the nation’s job numbers are estimated and processed. Unfortunately, President Trump’s firing of the head of the agency that compiles the numbers was motivated by the former, not the latter, and could leave us in an even worse position.

The media is abuzz over two negative developments in the U.S. labor market. First, are the recent and sharp downward revisions in the nation’s nonfarm payroll employment data, a correction that has left us with the weakest three months of job growth in the post-COVID economy. The second development, a result of the first, is the dismissal of the head of the U.S. Bureau of Labor Statistics (BLS) with an explicit accusation of malfeasance by the Trump administration. President Trump claims the new employment estimates are not reflective of the true health of the U.S. economy and that the negative revisions are politically motivated. Are these numbers indicative of a weakening economy, are they a reflection of corruption filtering into the public data creation process, or is something else going on?

While it’s difficult to surmise from Los Angeles what is actually happening in the halls of the BLS in Washington DC, we are familiar enough with the systems long used to estimate nonfarm employment levels to find the administration’s claim that the numbers were “fixed” to effect a particular political outcome extremely dubious. And, of course, the Commissioner of the BLS herself has no control over the process up to the point of never actually seeing the numbers until they are ready for release. The Commissioner’s firing, and President Trump’s nomination to replace her with someone viewed by many as a loyalist, is likely being driven by the administration’s desire to suppress anything resembling negative news on the economy—leaving businesses and households in the dark as to the actual state of affairs. But there are other important issues at play, including long standing problems with the BLS’s estimation and seasonal adjustment processes. That said, it is worth investigating whether the recent revisions are historically unusual and what the new data is really telling us about the economy.

Broken Not Corrupted

Drilling down, we see that the recent downward revisions in the data are unusually large, and this could be indicative of a slowing economy or a broken—rather than politically corrupted—data production process. As it turns out, the larger than normal revisions are not new—they have been going on for almost three years. This runs deep into the Biden administration and should confirm a lack of political intentions, but it still leads us to ask why the BLS has done nothing to fix what is clearly an ongoing and persistant problem. Ultimately, we agree with the Washington Examiner’s recent headline: “Trump made the right call ousting Bureau of Labor Statistics leader, but for the wrong reason.”

First, a brief overview of the BLS’s nonfarm employment data, otherwise known as the establishment data. This data represents one of the two major sources of employment information in the United States (the other source is the U.S. Census’ Current Population Survey from which we derive the unemployment rate). The BLS’s payroll data are linked to W2 employees and are derived from the unemployment insurance payments made by employers. Because the unemployment insurance data is lagged by 6 to 9 months, the BLS runs a survey known as the Current Employment Survey (CES) to create more up-to-date estimates.1 The raw data from the CES are weighted to create an estimate of total employment using benchmarks derived from unemployment insurance tax records and adjusted for seasonal patterns and business births and deaths. These preliminary estimates are released monthly and revised over time as more complete information become available from the unemployment insurance data, the CES survey, and seasonal patterns.

There are always numerous revisions to the nonfarm employment estimates. Even the current estimates will be subject to further revisions in the coming months—they won’t be completely “fixed” until sometime in 2026. To see an example of this in action, consider the estimate of the change in nonfarm payroll jobs from July to August of 2023. The initial estimate, released in September, was that 187,000 jobs had been added. In the October release, after estimates of the number of jobs in the previous three months were updated, the re-estimated change from July to August was that 227,000 jobs had been added. The following month more revisions were applied, and the July-August change fell to an estimate of just 165,000 jobs added. When new benchmarks were applied over the next year, the final estimate ended up suggesting the nation had added 157,000 jobs from July to August of 2023.

While 227,000 to 157,000 may seem like a giant swing in the estimate of job growth over a single month, it’s hardly unexpected given the limits of the systems used to collect the data. And, to be fair, the BLS does what is can with the budget it has—more accuracy could be bought, but that requires more money and given the nation’s extreme budget deficit, it’s unlikely that will happen any time soon. And it may not be necessary. Monthly variance in estimates tend to work their way out of the system over time. Additionally, a number of U.S. agencies collect a wide variety of data from a broad range of sources, all which help to build a more comprehensive context around the data points. The key thing to remember is that one month does not a trend make.

It’s Not About Who’s In The White House

So, what happened with the recent downward revisions? Well, first of all, the BLS didn’t just revise the last few months, they have been revising the counts down all year, with the largest revisions occurring in the last couple of months. Initial estimates were that the nation had added over a million jobs from January 2025 to July 2025—basically on par with the average pace of growth. The revised numbers now show a gain of just 597,000 roughly half of the average growth rate, hence the Trump administration’s accusations of foul play.

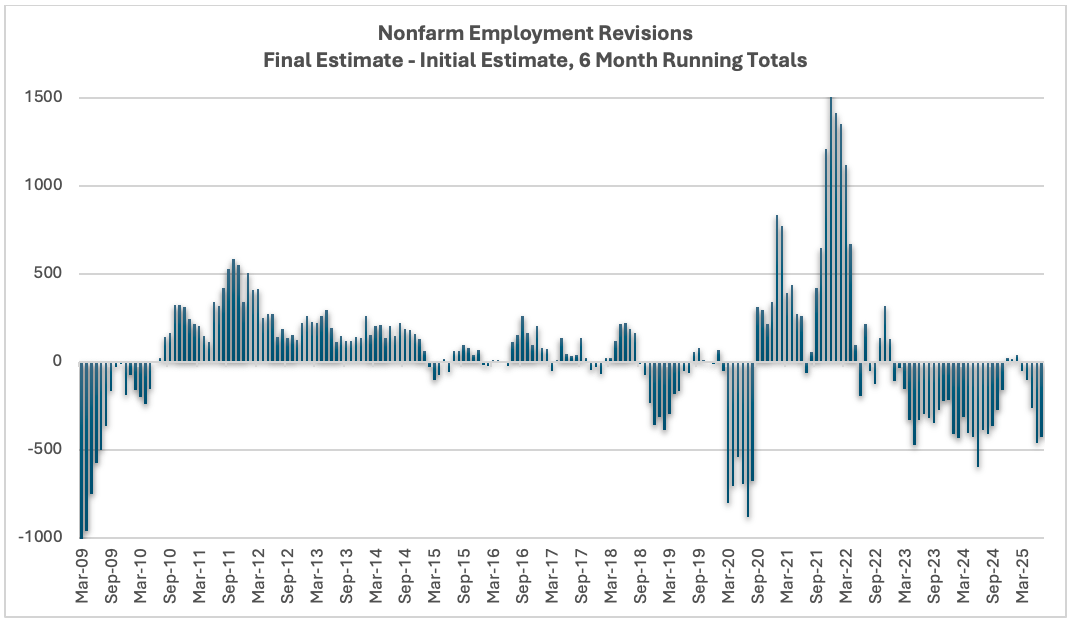

How unusual was this change? The answer is a bit muddled. The following graph shows the difference between the BLS’s initial and final estimates of job gains over a 6-month period using a running total. A negative number on this graph represents a downward revision, whereas a positive number is an upward revision. Historically, such large downward revisions are only seen around recessions due to the nature of the estimation system. The model typically overestimates job growth when the economy is slowing, and underestimates it when the economy is picking up speed. We saw this happen in 2020 at the start of the pandemic, and in 2009 during the Great Recession.

The recent revision may seem like big news, implying that the economy is tipping into a downturn, or as the Trump Adminstration claims (wrongly), that the BLS is somehow manipulating the numbers. But the historic pattern has broken down in the post-pandemic era and downward revisions have been happening almost continuously since late 2022. The data at the end of 2024 was unusual inasmuch as it wasn’t revised down at all. It is clear the BLS’s estimate model is struggling for unknown reasons. One clue may be that the rate of response on the CES has dropped from 60% to below 40%, although this would only explain the variation in the revisions, not the upward bias seen in the initial data over the last few years. What is clear is that 1) none of this has anything to do with who happens to be sitting in the White House, and 2) the issues with the BLS model are real and need to be fixed.

Is The U.S. Economy Really Slowing?

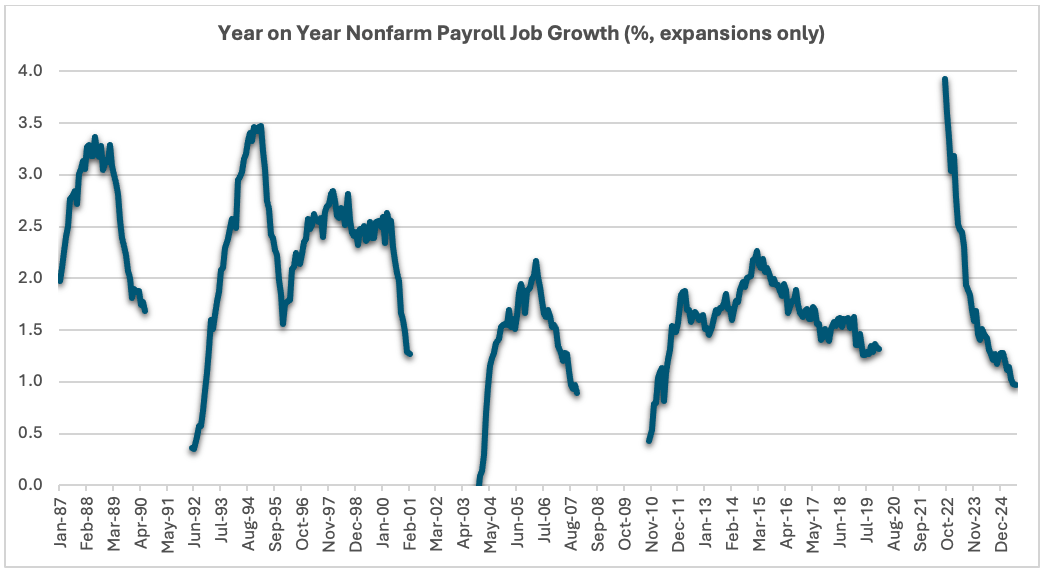

With all this in mind, it does appear likely that the recent slower growth numbers are the real deal—albeit there are still more revisions to come. What does it mean? It’s not good. The last time the United States tallied a mere 35,000 job gain per month for 3 months running outside of an actual recession was in the runup to the Great Recession—not exactly a comforting comparison given the current degree of uncertainty surrounding the health of the U.S. economy. Year-over-year jobs growth is now less than 1%, a number typically seen only in the context of a nation sliding into a recession (see graph below).

We can probably link some of the job slowing to the Trump administration’s policy turbulence and the subsequent moderation of consumer spending, fluctuations in trade, and stock market volatility. The nation did have a negative GDP growth rate in the first quarter of the year. And the sharpest declines in growth (comparing the average monthly job growth for the last 3 months to the previous 6 months) occurred in the government, manufacturing, trade, and transportation sectors. This suggests that DOGE and tariffs are having a substantially detrimental effect on U.S. employment. But that said, the nation has been experiencing a general deceleration of employment since 2022, with only a brief respite at the end of 2024. The recent slowing doesn’t suggest a change in the growth trend, but a continuation of it.

With that in mind, there are a few other data points that need to be considered before we even start talking about an oncoming recession. First, the slowdown in employment data is not occurring alongside any other signs of weakness in the labor markets. Initial claims for unemployment insurance, for example, remain in the same 200,000 to 250,000 range they have been in for the last few years, and the unemployment rate itself remains just a hair above 4%—considered full employment by most economists.

Equivalently, the data on job separations and job openings from the BLS’s Job Openings and Labor Turnover Survey (JOLTS) have also remained in normal ranges over the last few years. This suggests that the slowing of job growth isn’t being driven by layoffs or a major slowdown in labor demand. While there have been a lot of headlines trumpeting the labor market issues facing new college grads (they have a current unemployment rate of 8.5%), we saw similar levels of joblessness among this group over the last few summers (note that this could be driven as much by picky job seekers as it is by picky employers). The bottom line is that we don’t see anything in these data points that broadly concerns us, hence it’s difficult to believe the employment numbers will cast much of a shadow over the current economic expansion.

Worker Shortage Is The Problem, Healthy Immigration Is The Answer

Another reasonable explanation may simply be that we need to wait for more employment revisions. A problematic pattern we’ve seen in the data over the last few years is that payroll employment growth has slowed during the summer months despite seasonal adjustments that should remove such wrinkles. This can be seen in 2024 and 2023 as well as in the current slowing. It suggests that something is amiss with the BLS’s seasonal adjustment process—hardly surprising given the broader problems in the estimation process—and explains why jobs growth was so strong during the 6 months preceding the recent slowdown when the annual pace was well over 2.2 million jobs. This also suggests that better job growth will be revealed in the months to come as the data moves back towards its actual level. And of course, eventually, the seasonal adjustments will be fixed and the strange ripples we see now will be ironed out of the data completely. This indicates that the U.S. economy has been decelerating to a new, steady, lower pace of job growth (in the low 1% range) ever since its recovery from the pandemic, revealing an even bigger problem—the overall slowing of long run job growth despite solid labor demand. And that, my friends, sounds like a labor supply problem, something the nation has faced in recent decades due to a decline in birthrates.

The only way to offset this decline is to import new workers—otherwise known as immigration. But given pall that has fallen over foreign migration due to the reelection of Donald Trump, this may end up being a new-normal for job growth for the rest of his administration. We should be able to see this in the Curret Population Survey, but the CPS also has problems with its estimate of labor force given the unclear data on the pace of undocumented migrants entering the nation and its work force. It takes new Census data to revise the CPS and that won’t happen for years given the lag on these surveys.

The Last Word

To sum up, there is no conspiracy here, but there is an estimation problem—one that should have already been addressed by the BLS. Of course, the ‘wrong reason’ for firing the commissioner, as the Washington Examiner headline asserts, may be that President Trump wants to choose a new BLS head not to create better estimates, but to create estimates the President finds more politically favorable. That’s far from better. And as for the weak new estimates themselves, we do not believe these are being driven by an economy tipping into a downturn, but rather by an economy running out of workers—a likely byproduct of the Trump administration’s intense anti-immigrant stance.

(1) This is a monthly survey of approximately 119,000 businesses and government agencies covering about 629,000 individual worksites. This survey collects data on the number of jobs, hours worked, and earnings from a sample designed to represent all nonfarm industries across the U.S. economy. The final estimate reflects the number of jobs (not workers), meaning one person with multiple jobs is counted once for each job held.

-

See more

14 August

See more

14 AugustConspiracy, Truth, or Something Else: Untangling the Employment Decline

-

See more

22 November

Who Should We Credit For Trump’s Big Win? Jerome Powell

-

See more

6 August

U.S. Labor Market Fears and the Global Equity Swoon

-

See more

30 April

Surge Pricing Vs. Dynamic Pricing: What’s In A Name? As It Turns Out, A Lot!