Author

The red wave that swept Donald Trump to a second term took most everybody by surprise. Unsurprisingly, the big win has sparked vitriolic finger-pointing within the Democratic party, a sense of elation within the Republican party, and panic in political pollster circles, where yet another big miss has been notched. However, it’s easy to over-interpret what this means for the U.S. economy and “our democracy” moving forward. Many are interpreting the sweeping win as a mandate to enact the Republicans’ platform. Yet, a cursory look at the data shows it is more likely a reflection of voters acting on that age old question: What have you done for me lately? Realistically, the Democrats never stood a chance—not because of their platform, but because of prevailing social narratives about the U.S. economy.

First, appreciate that while the edges of the political spectrum are the noisiest, they are not the driving force in election outcomes. As the platforms of both major parties have become more polarized in recent decades, a greater share of the population now declare themselves Independent—43% according to Gallup in 2023. Most Americans don’t like either party. It is this neutral mass in the center that determines the outcome of major elections.

This dynamic has led both parties to approach elections by throwing endless policy fishhooks into the middle, hoping to pull some of these centrist voters in their direction. While this competitive fishing contest captures the attention of the media and pollsters, it’s secondary to the bigger picture. What the mass in the middle really cares about is whether they feel better off than they did four years ago—yes, that old canard. If the answer is “no,” then it’s time to throw the bums out and try something new, regardless of what that “new” might actually be.

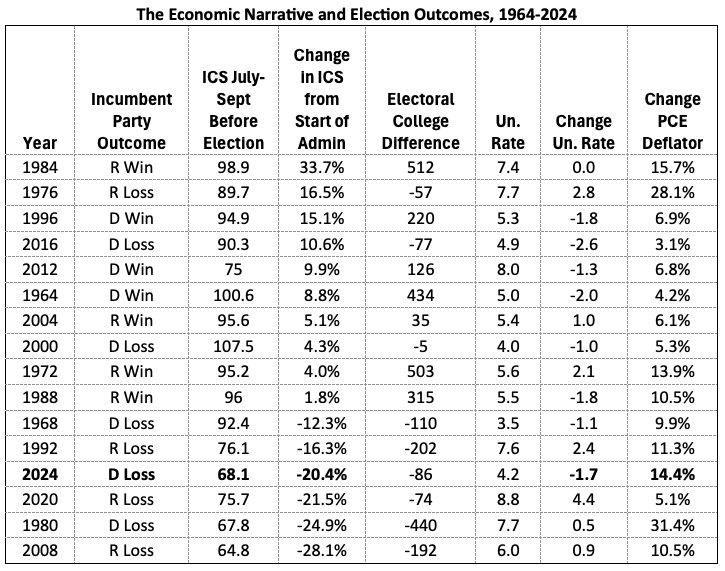

If this sounds crass, it’s a view that aligns almost perfectly with the data. Consider the University of Michigan Index of Consumer Sentiment (ICS) as a simple measure of the current social narrative about the health of the U.S. economy. Then consider how the change in this metric over the course of any one presidential administration relates to election outcomes. Specifically, we look at the change in the ICS from the second quarter of a new administration’s term (post-honeymoon) to the last three months before the next election (up to September). We then compare this change to whether the incumbent party won or lost the election. The table below shows these sentiment changes, ranked from highest to lowest, for the last 16 U.S. presidential elections.

In 10 of those election years, the ICS rose over the course of the incumbent party’s administration, ranging from a low of 1.8% during Reagan’s second term to a high of 33% during his first. In 7 out of those 10 contests, the incumbent party won the election, suggesting that better times can help the incumbent party, but do not guarantee success. Losses to the incumbent party happened in 1976 (Ford), 2000 (Gore) and 2016 (Clinton). It is worth noting that these three losses were very close (3 of the 4 tightest races). The wins in the other seven elections were clearcut.

On the other hand, whenever there was a sharp drop in the ICS during an administration, the incumbent party lost, running 0 for 6, and usually by a wide margin. It is worth noting that both Democrats and Republicans have suffered equally from such declines, splitting the losses across these 6 bad runs. This pattern held true for the last two elections, affecting Donald Trump in 2020 just as much as it hit Kamala Harris in 2024—albeit the sources of the decline in sentiment were different in each case. Trump was hit by the pandemic downturn and Biden by the inflation narrative. In both cases, even if there had been a strong candidate and a polished platform, the incumbent party likely would have lost. The data tells us that the result of the 2024 election should have been largely anticipated (and in some betting markets, it absolutely was).

The takeaway is clear: a candidate’s policy platform doesn’t seem to matter much. When consumer sentiment falls over the course of an administration, the incumbent party is almost certainly going to lose; if it rises, they have a pretty good chance of winning. This brings us full circle to the well-worn phrase: “It’s the economy, stupid.” And exit poll after exit poll for this election repeatedly show that the economy, particularly inflation, is one of the main reasons people chose the Republican ticket.

And this is where things start to get interesting. We can see how the gap that sometimes exists between narratives about the economy and what is actually happening can have critical effects on the course of political and economic history. In many of the 6 losses it’s easy to explain the decline in consumer sentiment by the very real decline in the economy. For example, the decline in sentiment over the course of the Carter administration can be linked to the misfortunes of an economy beset by inflation and to then Fed Chairman Paul Volker’s even worse cure, which set off the recession of 1980. The decline in sentiment at that time reflected true economic distress.

This time, in contrast, the U.S. economy has not been doing badly. In fact, it has been performing well. The unemployment rate is still just 4.2%, real GDP growth has been strong, and both real incomes and net worth are rising, even as consumer debt-to-income and debt payment-to-income ratios have fallen to the lowest level in decades. The decline in consumer confidence also accompanied a leap in the stock market to all time high levels. Americans, at least on paper, seem to have very little to complain about—but they were indeed unhappy, much to the dismay of the Democratic party.

There is little mystery as to the source of today’s negative sentiments—the bout of inflation from 2021 to 2023. It’s important to remember, however, that these price hikes were fueled by a surge in consumer demand—driven in turn by subsidies and by the massive asset bubble created when $5 trillion in quantitative easing (QE) was unleashed by the Federal Reserve during that time. Consumers weren’t victims of inflation; they were the ones who caused it. But the fact that consumer sentiment fell as their own higher demand drove inflation clearly shows that consumers see it the other way around.

As noted in another recent commentary from Beacon Economics, inflation seems to exert an outsized influence on consumer sentiment—outsized in the sense that rising prices have a more negative effect than an equivalent rise in incomes. In other words, if prices and incomes both increased by 5%, leaving consumers technically in the same position, consumer confidence would still decline—the increase in prices seems to exert a heavier psychological cost. This bias precisely explains the dichotomy between the narrative and the reality of today’s economy—and the red wave that has now left President-Elect Trump with control of both the House and Senate.

What caused the jump in inflation? As Milton Friedman famously stated, “Inflation is always and everywhere a monetary phenomenon.” We need look no further than the 40% increase in the U.S. money supply that occurred between 2020 and late 2021, courtesy of $5 trillion in QE. Yes, Trump’s big win in 2024 can be attributed mainly to the Federal Reserve’s choice to massively overreact to the pandemic in 2020. How wonderfully ironic, then, that the President-Elect has made no effort to hide his disdain for Fed Chairman Jerome Powell—the man he originally appointed to the role —who seems to have inadvertently helped Trump so forcefully reclaim the Presidency.

This begs the question: could the Democrats have done something to help consumer sentiment rise faster? Was there some magic marketing elixir that could have given them the needed lift? Quite a few pundits have asked why the Democrats didn’t try harder to illustrate how well the U.S. economy was doing—but that’s a difficult message to convey off a progressive, redistributive platform. And it points to a broader issue we must confront—whether the narrative can be actively manipulated, independent of real economic influences. It’s a bit like asking whether the active efforts of Russian and Chinese agents to sow misinformation on U.S. social media sites have managed to influence consumer sentiment, and, by extension, our election outcomes. It’s hard to say. As social scientists, we still don’t fully understand how certain false narratives take hold and spread.

It does seem as though consumer sentiment reacted more negatively to inflation this time than it did back in the 1970s, when theory would suggest the opposite—today’s higher real incomes and savings should mean that inflation has less impact on the American narrative. One could argue that social media, misinformation, and the polarization of news media have caused the greater-than-expected effect. But then again, it might simply be that the United States has not seen any inflation for a long time and people simply aren’t used to it. Hence, they reacted viscerally. Clearly, this calls for more thorough study.

The bigger question is what it all means for 2028. Will Trump leave his party with enough momentum for another win? If the next four years prove stable and calm, it seems likely, since consumer confidence will likely rise over the next couple years as the inflation shock fades. But with that said, such a scenario is far from certain. Trump’s proposed policies, including tariff-induced trade wars and mass deportations, could create large disruptions. On top of that, the ballooning federal deficit and the asset bubble that swelled even more after the election are challenges waiting to unfold. The Democrats might have a chance to roar back in 2028—though they could end up inheriting an economy reminiscent of the chaos Barack Obama faced in late 2008. Be careful what you wish for—it just might come true.