Part 1 of this post (published last week) argued that the strong economic recovery the United States experienced in 2020 signifies that there is little real need for additional government stimulus. It also pointed out that the first stimulus package cost the nation $3 trillion but ultimately has played only a minor role in the economic rebound to date. The first stimulus’s remarkably little impact is due to the fact that it fire-hosed financial support across the entire economy as opposed to focusing efforts more narrowly on the parts of the economy suffering direct harm. As such, a very large share of the money ended up filtering through to the financial system in the form of debt reduction, increased savings, or for purchasing stocks, homes, and other assets. It will be counter-productive for the United States to engage in another stimulus package.

Key Points:

- The structure of the stimulus efforts means most of the money flows into the financial system rather than to current spending, reducing its intended and immediate value of growing the economy and creating new jobs.

- The U.S. economy has already recovered substantially from the pandemic-driven downturn and has plenty of momentum coming into 2021. Moreover, the impact of the first stimulus on savings and bank deposits will provide the necessary fuel to help the nation reach full recovery now that effective vaccines are being distributed and the virus is being brought under control.

- More stimulus will be potentially destabilizing for the U.S. economy. In the short-term. this cash could drive another asset bubble or create inflation. In the longer term, the massive increase in the Federal debt will drive up real interest rates and push the United States significantly closer to a fiscal crisis.

Where did we go so wrong? The U.S. Congress acted fast to support the sagging economy at the start of the pandemic. But when crafting policy, like car racing, speed without accuracy can lead to disastrous results. Consider what happened under the three major programs in the first stimulus package—the expansion of unemployment, the PPP program, and direct payments to families—which totaled about $1.6 trillion in spending. [NOTE: Many of the more targeted sources of relief spending—supporting hard hit local infrastructure such as airports and metros, expanding food support, and all funds used to control and eliminate the COVID-19 virus—clearly had high value for the economy.]

Because it targeted those who were directly harmed, expanding unemployment was clearly the best way of helping workers who lost their jobs and income due to the pandemic. But in implementation there were serious problems and inefficiencies. The rush to get those unemployment checks out led to the potential for massive fraud, and that potential was realized. In California, the total amount of invalid payments could come in as high as $30 billion according to some estimates. We can only guess at where the national total will ultimately end up.

PPP loans were, in theory, a logical way to help small businesses experiencing short-run hits to their revenue streams. The idea was that this money would assist businesses that didn’t have the capital to make it through to the other side of the pandemic. Yet, again, implementation was the problem as there was little effort to direct the money to truly needy businesses. Instead, it was doled out largely on a first-come, first-serve basis, meaning that an enormous share of the PPP loan money went to firms that had their banker on speed dial – those are highly unlikely to be the small businesses in need. A report from the Washington Post, using data from the U.S. Small Business Administration, finds that a full quarter of the funds went to only 1% of applicants [https://www.washingtonpost.com/business/2020/12/01/ppp-sba-data/].

Of all the policies put into place in the first stimulus package, the least useful, and thus the worst use of funds, were the direct payments. This entailed simply mailing a huge proportion of the U.S. population a check for $1,200, with an additional $500 for children. In the first stimulus package, over 153 million payments were made by the IRS amounting to well over $260 billion – all paid for through new Federal government debt. This program has also been the center of the debate surrounding the second stimulus package (proposed $600 checks) and now the third (proposed $1,400 checks), with total costs rising well above a half a trillion dollars depending in the structure of the third package.

U.S. politicians have been keen to spend this money because it is, not surprisingly, popular. A recent focus group of both Donald Trump and Joe Biden voters showed a huge divide with one major exception—both sides agree that we need more stimulus checks [https://www.businessinsider.com/video-frank-luntz-focus-group-unity-goes-off-the-rails-2021-1]; after all, who doesn’t like free money!

But this money is anything but free. The costs of the programs currently being proposed combined with the earlier programs could saddle the United States with over $6 trillion in new Federal debt in just two short years. This is an amount that will push net Federal debt to GDP from the 75% range to well above 100%, a line in the sand that when crossed, most economists agree looks very worrisome.

Generations of our children and grandchildren will have to pay this back plus interest through higher taxes and reduced government benefits – all to fund ‘free money’ today. It will have the added effect of driving up interest rates in the near term, reducing the ability of the Federal government to respond to the next crisis, and in all likelihood, is part of the reason asset markets look dangerously hot right now. And remember, the long-run budget situation was already grim pre-pandemic due to the rising costs of Federal entitlement programs. We are moving the day of reckoning forward in time at an alarming pace. The September 2020 Congressional Budget Office debt forecast has Federal debt held by the public approaching 200% of GDP by mid-century, and this doesn’t include the current stimulus plan being promoted by the Biden administration, Democratic lawmakers, and some Republicans.

The argument for direct payments is that many people are in desperate need of the funds. Without this money—so goes the logic—consumer spending will stagnate, the economy will remain stalled, and ultimately this lost growth, along with the sheer scale of human misery, will hurt future generations more than the debt we are incurring in the short run. Sure, proponents argue, some of the funds will go to people who haven’t been directly impacted by the pandemic—but even here the increase in spending will help the economy get moving. In short: this is a worthy investment, albeit one our generation won’t have to pay for (lucky us).

Unfortunately, this sort of stimulus critically depends on what people do with the money they receive. The assumption is that it will be immediately spent, driving business revenues and supporting jobs. But this isn’t how consumers are behaving. The large decline in consumer spending that occurred over the past year was driven not because consumers were unable to buy goods and services, but because those goods and services were unavailable for purchase because of the pandemic. Giving more money to families when they can’t spend money is a pointless endeavor from a short-run perspective. The only place direct payments have an immediate impact is in helping those who have lost income due to the pandemic—the unemployed.

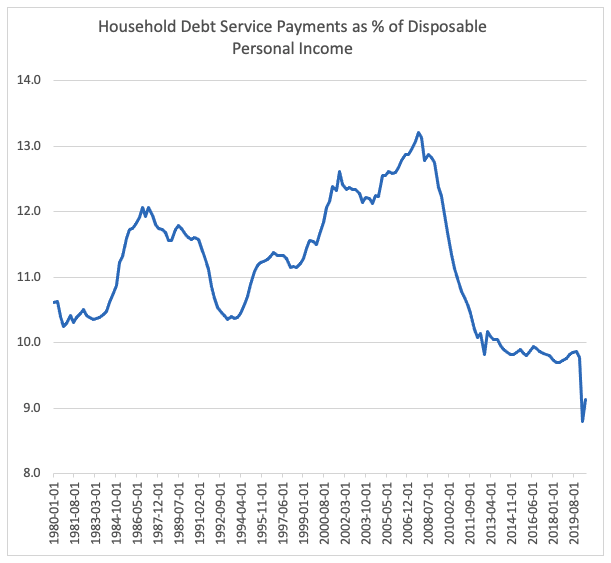

Consider data from the Federal Reserve. The New York branch produced a special June supplement of their consumer spending survey that showed only 18% of households that received cash spent the money on essentials, while another 8% bought what they called non-essentials [https://libertystreeteconomics.newyorkfed.org/2020/10/how-have-households-used-their-stimulus-payments-and-how-would-they-spend-the-next.html]. As for the balance, over two-thirds, it was used to pay down debt, or just saved. No jobs were supported, no businesses were saved from bankruptcy, no hungry families received critical nutrition. Overall debt servicing levels (debt payments as a % of income) in the United States were already at an all-time low prior to the pandemic. Today’s families were enriched at the expense of future ones through a process of swapping personal debt for public debt. This isn’t stimulus as much as it is an intergenerational mugging.

The PPP money can be similarly critiqued. The idea was to give money to businesses who didn’t lay off workers. Theoretically this is a problem. Laying off a worker carries substantial costs to a business—from the loss of human capital to the disruption of normal operations to the impact on morale; it is usually only done as a last resort. It seems unlikely that covering two months of pay would do much to protect an endangered position, except maybe keep it around for a few extra weeks.

But the real problem was that there was no real effort to ensure that the money went to firms where it would truly have made the difference between laying workers off or keeping them on payroll. Instead, it went to businesses that were able to react quickly, those with a close relationship with their banker and accountant. As such, much of the PPP cash assuredly went to business owners who, like consumers, used it for savings or debt reduction.

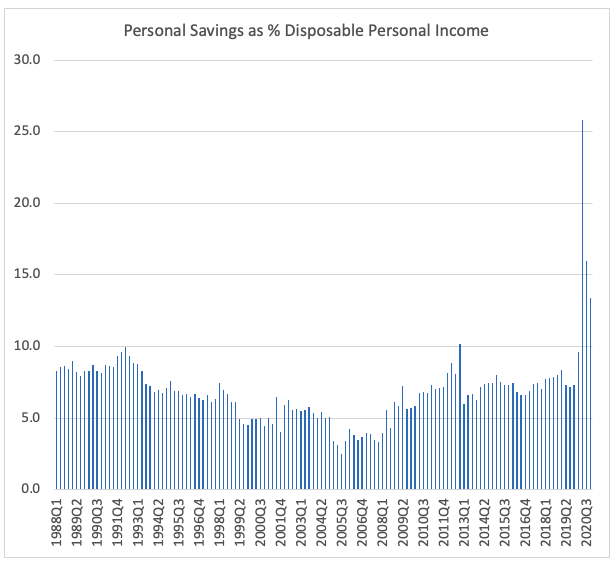

That the first stimulus package did little for the economy in 2020 is obvious in the data. The household savings rate shot up to levels never seen in the history of the United States: 25% in the second quarter and a still high 13.4% by the end of the year. This was not driven by the stimulus alone but also by the fact that spending dropped significantly more than incomes, implying that savings would have risen sharply even without the stimulus. In total, U.S. households saved $1.6 trillion more than they would have without the pandemic and stimulus; that’s well over half the size of the first stimulus package.

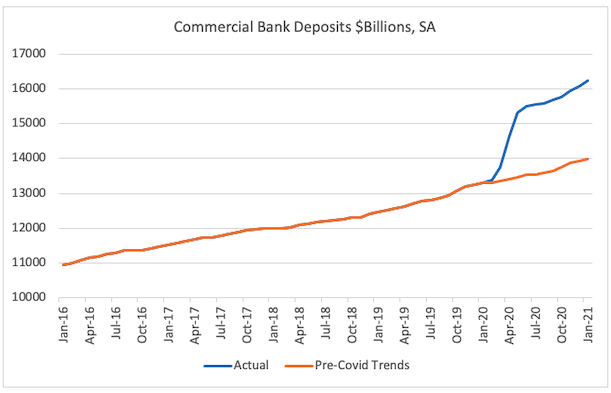

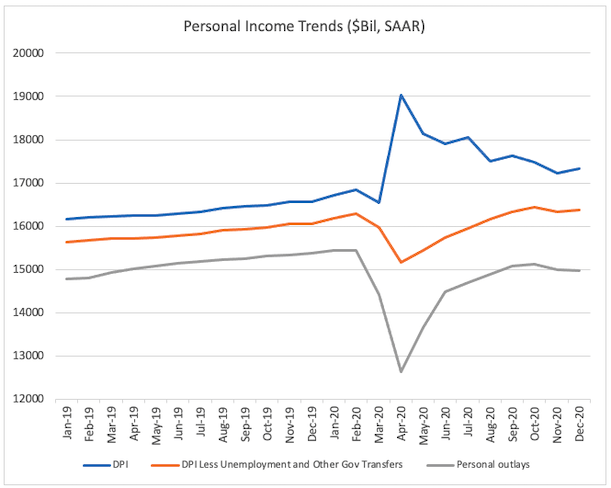

The net result was that despite the slowing economy, aggregate disposable personal income in the nation actually surged during the year, with government payments offsetting earned income losses by 2 to 1 – helping us to understand the massive surge in savings. Where has all this cash landed? Commercial bank deposits swelled like never before, increasing by $3 trillion in 2020 over 2019 levels; recent trends would have suggested only about $700 billion in growth. This $2.3 trillion dollar jump over trend is just slightly less than the $2.5 trillion cost of the first stimulus program.

This pass-through meant that, on-net, the first stimulus provided, at best, modest support in helping the U.S. economy rebound last year. That rebound happened naturally due to the mitigation efforts of consumers and businesses. However, the first stimulus will help the recovery this year. The two trillion in cash reserves represents significant pent-up demand that will start to bubble to the surface as we gain control over the virus, and the parts of the economy that remain constrained—recreation, hospitality, travel—begin to fully reopen.

One of the arguments in favor of another round of stimulus is that it supports the long-run objectives of the new White House administration. The New York Times makes this conflation of goals obvious when it suggested that direct payments are needed because of “the long-term effects of slow-growing incomes and wealth over the past four decades” and because “[i]t’s surprisingly progressive” [David Leonhardt. (2021, January 28). The debate over the checks. The Morning, New York Times.]. Indeed, there has been a recent push by Democrats to include a hike in the national minimum wage as part of the stimulus bill—something that would seem counter-productive to driving better employment growth.

While we can quibble about the underlying premise regarding slow-growing incomes (not to mention that it’s no surprise flat payments are by definition a progressive policy), the real issue with this justification is that debt-financed fiscal stimulus is medicine for business cycles, not long-run economic development goals. Reducing income and wealth inequality in the United States is an important policy goal, but such efforts need to be paid for through increased taxes or reduced public spending elsewhere, not a massive expansion of government debt. The history of the world is full of debt-fueled “development” plans that ultimately left nations worse off. And while the stimulus checks are progressive, the poorly implemented and significantly larger PPP program was very regressive, given that business owners are typically considerably wealthier than the employees who work for them.

And fire-hosing money across the economy carries its own risks that need to be factored into the calculation. Economic instability is always harder on lower-income families. If one of the goals is to help these families in the long run, we should work to reduce potential instabilities. The stimulus packages being proposed will do the opposite. It will over-stimulate the economy, which while feeling good in the short run, will ultimately create new imbalances that will have negative repercussions down the line. Remember how good the economy felt in 2006 when it was being juiced by the sub-prime credit bubble, and how bad it looked two short years later?

If you want a simple metric illustrating how over-the-top the stimulus efforts have been, consider that in 2020 the pandemic reduced aggregate output in the United States by $1.1 trillion and yet the Federal government spent $3.4 trillion on stimulus. In 2021 the government are proposing nearly $2 trillion more in response to what is likely to be a half-trillion-dollar deficit in output. We’re already seeing the impact of too much stimulus on the red-hot stock and housing markets, conditions that may well morph into a dangerous bubble in the coming year. And all this cash will make inflation more likely when combined with the Federal Reserve’s similarly aggressive stimulus policies. We may well be doing vastly more harm than good by continuing this bizarre push for more stimulus.

Almost humorously, the New York Times piece also suggested that a good justification for another round of stimulus checks is that they are “simple.” This is true, but it might be better stated as “simply wrong.” The economy is already recovering. And there is plenty of pent-up demand to get things moving once the virus is under control. Moreover, all this free cash is already creating economic imbalances. Ultimately the government should not and cannot be the 100% insurer of cyclical economic risk. Such funding should be limited to disruptions that pose systemic issues for the broader economy, and there is little evidence the U.S. economy is at such a juncture.

These quixotic stimulus efforts are being driven by the same root cause—the ‘miserabilism’ that has so afflicted the nation’s psyche over the last decade. That is the need to constantly exaggerate the negative while ignoring the positive regardless of actual circumstance. Assuming that every problem is an existential crisis is at the root of the poor policy choices now being pursued as well as the radical populism that has so divided the nation politically. This is the ultimate risk of miserabilism, in our rush to fix something that isn’t broken, we may well end up breaking it.