Today’s big news was that the Federal Reserve only raised the Federal Funds Rate by a quarter point and has seemingly backed off on its plans for future interest rate hikes. Is this good news or bad? Oddly, the news first caused equity markets to rise, then fall. Why such a mixed reaction? Because the Fed didn’t actually address the issue at the heart of the banking crisis, and because of that, we still don’t know where things are heading in the world of credit.

Two weeks ago, Fed Chairman Jerome Powell announced that inflationary pressures had not cooled enough, and that the Board would likely be raising rates more than originally anticipated. These few words set off a chain of reactions that led to the current banking crisis, including the forced closure of two large banks and enormous stress on many others.

The markets were betting that this current stress in the banking system would force the Fed to back off on rate increases—the exact opposite of what Powell foreshadowed. Today the Fed met to discuss monetary policy, and sure enough, they pushed rates up by only a quarter point (a half was expected) and have strongly suggested they will now pause any additional increases. Interest rates dropped as a result, with the 2-year treasury dropping below 4% for the first time since last September. You would think this would have given the markets a boost. Why did they waffle? Because, as it turns out, the Fed didn’t actually do anything relevant in regard to the banking crisis.

As noted in previous writings, the U.S. commercial banking system is as clean today as it has ever been, with overall loan delinquencies at record low levels. The stress in the banking system did not start with problems in the loan portfolios of commercial banks as it did in past banking crises, but rather with sharp changes in Fed policy over the last three years. In a nutshell, the process went something like this:

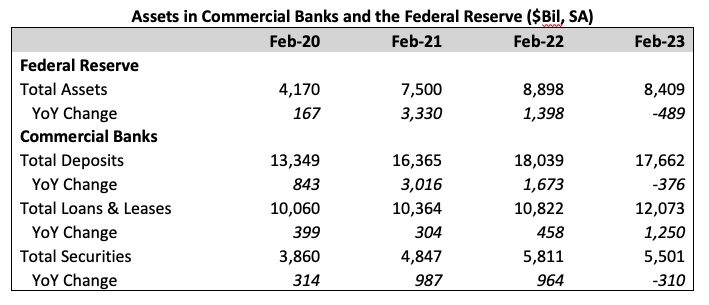

- The Fed overreacted to the pandemic by issuing $4.7 trillion in new money through QE in just two years (Feb 2020 to Feb 2022). That cash was then helicopter-dropped across the economy by Congress through a variety of spending programs.

- The money created by QE ultimately ended up in the banking system, leading to a $4.6 trillion (roughly 35%) increase in banking deposits across the nation’s commercial banking system.

- The banks used $2.7 trillion of these new deposits to buy securities and make loans. The balance was held as cash or used to pay off other liabilities.

- In response to inflation, over the last year the Fed has raised interest rates sharply through the Federal Funds rate. These interest rate increases have reduced the resale value of loan and security assets on the banks’ books.

- Additionally, over the past year the Fed also began the process of quantitative tightening—reducing their balance sheet by $500 billion via the sale of treasuries and GSE debt that they had purchased in 2020 and 2021. This decline has caused the commercial bank deposit base to fall by $400 billion.

It is these last two steps that have partly caused the financial stress in the U.S. banking system, albeit in different ways. News coverage has primarily focused attention on the traditional tool in the Fed’s basket, the Federal Funds Rate. But the real story for the banks right now is the Fed’s use of quantitative easing and tightening (QE and QT), and on this we have no information about the Fed’s future plan.

The Fed’s change in policy from loose to tight began roughly a year ago, in response to the increase in the pace of inflation. Much to their chagrin, the U.S. economy has remained healthy, consumer demand continues apace, and the result is that there continues to be demand for debt. As a result, despite the increase in interest rates over the past 12 months, outstanding loan balances at commercial banks have grown by $1.25 trillion—good news since these new loans are at a much higher interest rate and, hence, can ultimately help bank profitability in the medium term.

But at the same time that rates have been rising, QT has caused a big problem for bank balance sheets. The sale of bonds by the Fed, and the subsequent decline in the money supply, caused a drop in deposits in the banking system. The result of increased demand for loans and falling deposits meant that many banks quickly burned through the cash reserves they had built up during the QE phase. Some banks, such as Silicon Valley Bank, saw large enough declines in their deposit base that they were forced to either look for new (very expensive) external funding, or worse yet, sell existing assets on their books at now reduced prices because of the higher interest rates. Neither option is good as both hurt profitability and thus cause a reduction in a bank’s equity cushion. Eventually, this set off a number of classic bank runs.

So, there are two points of stress on the banking system today. First is the diminished value of existing assets on banks’ books from the last few years due to higher interest rates. Second is the decline in deposits, which is causing these losses to be realized from an accounting standpoint. A change in the Federal Funds Rate now is largely meaningless. The only real question is whether the Fed will continue to shrink the bank deposit base through additional QT—something that was not discussed today at all.

Realistically, even if the Fed had reduced the Federal Funds Rate by half a point, but continued their QT process, it seems likely that more banks would be subject to runs. After all, declines in deposits can only be offset by selling securities and loans that are on a bank’s books at a loss. Equivalently, if the Fed had raised the Federal Funds Rate a full half point but actually engaged in modest QE, then the expanded deposits would allow banks to avoid realizing losses and sharply reduce the risk of runs.

As it is, take off the party hats, put away the noise makers, and put the champagne back in the cooler. Today’s Fed news was really no news. Until we understand the direction the Fed is going with its quantitative tools, and the impact on bank deposits, we cannot predict if the banking situation will improve or get worse.